Consumer Health

Shape the future of consumer health.

The consumer health industry has been extremely resilient through the last three years of COVID-19. Growth never slowed even during the peak of the pandemic as categories like Vitamins, minerals and supplements (VMS) stepped in to cover for the shortfall across Cold/flu and Pain categories, during times of lockdown and social distancing.

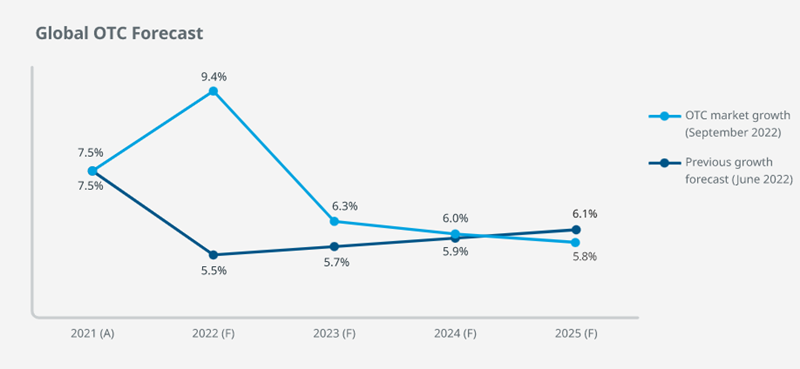

As countries and retail begin to return to normal in mid-2021, growth across the overall consumer health market accelerated beyond pre-pandemic levels. For the current MAT Q2 2022, the industry is tracking at +11.3% value growth (Exhibit 1) and remains poised to continue at +6% growth during the next 5 years. In 2022, we are also seeing the positive impact of above-average inflation and some pent-up demand from previous years. These effects will taper off starting Q4 2022.

Key drivers behind the separation of Consumer health business units are well known and the growing importance of self-care and over the counter (OTC) medications has never been greater. Strategically, firms have been focusing on investing in the pharma pipeline and thus leaving little space to invest adequately in consumer health business opportunities. We have also noticed that several consumer health firms were unable to secure deals for potential growth opportunities or smaller firms due to price-tags been deemed too high, leaving the way open for non-pharma players to swoop in and take the opportunity.

In closing, we are positive and excited about the recent announcements from both GSK Consumer (Haleon) and J&J consumer (Kenvue). For an industry that is healthy and continues to project a strong performance for the next 5 years(Exhibit 4), the announcements and formation of these new entities cannot come at a better time!

As Prasanna Pitale, Senior Vice President of IQVIA Consumer Health recently said: ‘The future for Consumer health industry has never been brighter and the new stand-alone consumer health firms will further strengthen the industry’s commitment to self-care.’

Shape the future of consumer health.

Illuminate a path to consumer health success

Adapt fast, maintain momentum and stay relevant

See how we partner with organizations across the healthcare ecosystem, from emerging biotechnology and large pharmaceutical, to medical technology, consumer health, and more, to drive human health forward.