In continuation of IQVIA’s Inflation Reduction Act thought leaderships series, the following is the third in a five-part blog series analyzing the first 10 products selected for Maximum Fair Price (MFP) negotiations. These 10 products represent the first of up to 100 products scheduled to be negotiated between 2023 and the end of the decade. The overall economic impact of the first 10 products belies the long-term impact on the life sciences industry, which will only grow as more products are added to negotiation.

Impact on Patient Cost Exposure

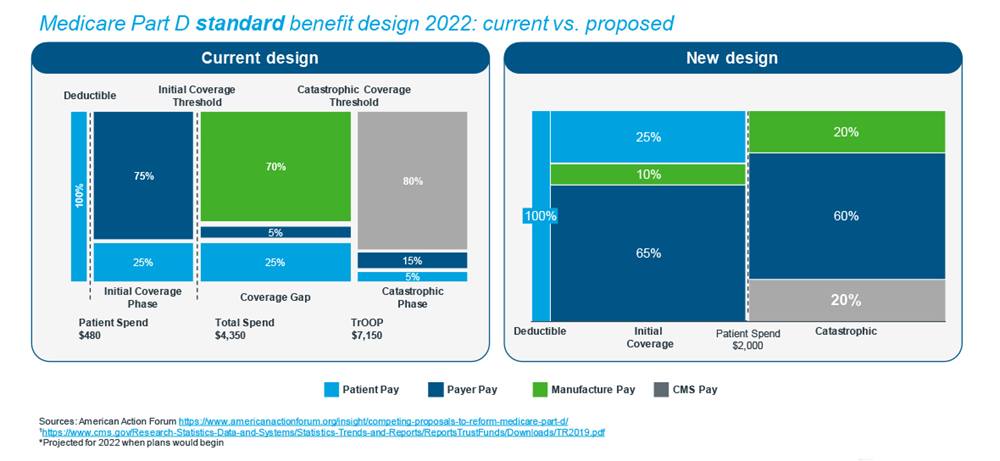

Patients will benefit from lower out-of-pocket (OOP) cost exposure as patient OOP will be set off the lower MFP price versus the higher list price. However, many patients are already exposed to low copays if they are Low Income Subsidy (LIS) patients, are in Employer Group Waiver Plans (EGWPs), or are Standard Eligible patients exposed to flat tiered copays rather than ones that are tied to a percentage of list price. Additionally, Standard Eligible patients will benefit from a simplified benefit design when the $2,000 annual out-of-pocket maximum is reached and will see their catastrophic copay requirements drop from 5% today to $0.

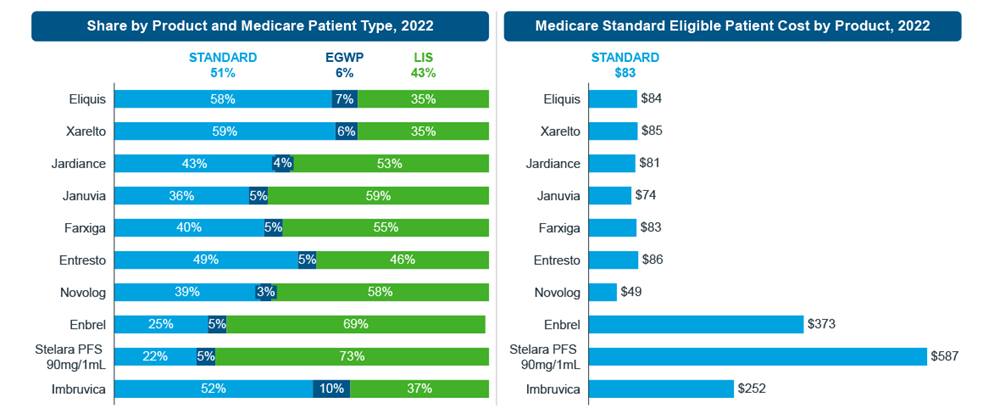

To understand the true impact of patients benefiting from Maximum Fair Price negotiations lowering drug prices, it is important to examine where patient cost exposure falls today across the three types of beneficiaries. Across the 10 selected products, the range of LIS exposure varies from 33% to 73%, with an average of 43%. These patients already pay low copays, so they will not see any impact on what they are being asked to pay under the Inflation Reduction Act. In fact, because of expanded LIS eligibility under the provisions of the IRA, more patients will benefit from this aspect of Medicare in the future.

EGWP beneficiaries, in general, also have lower out-of-pocket costs, as a beneficiary’s employer partially subsidizes drug coverage. Although shrinking over time, this group currently accounts for 6% of patients for the initial group of selected drugs. In total, the LIS and EGWP patient distribution means that approximately half of the beneficiaries for the first 10 MFP drugs are already exposed to prices below which the IRA would be impactful.

Although the degree to which patients save varies by brand, it is the Standard Eligible patient who is most likely to see costs capped at $2,000. To understand the impact of the $2,000 annual out-of-pocket cap, it is necessary to look beyond beneficiary type and current copay exposure as Medicare Phase of Coverage for Standard Eligible patients is also changing as part of the IRA.

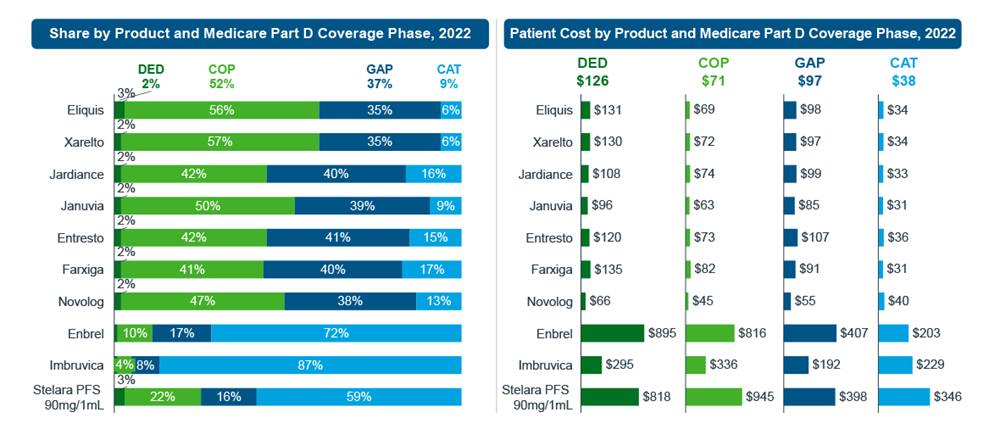

For the top 10 products, a good surrogate of when a patient will reach the $2,000 out-of-pocket cap is to identify those who are currently consuming these products while in the Catastrophic phase of coverage under today’s benefit design. This would represent the upper bounds of beneficiaries who would benefit and as is clear from the analysis, skews heavily towards the higher cost specialty products. For the three specialty products selected for negotiation (Enbrel, Stelara, Imbruvica), between 80-90% of Standard Eligible consumption is occurring in the Catastrophic phase of coverage where patients are currently responsible for 5% of the drug cost.

If you take Enbrel as an example of how this plays out in real life, we see that only 25% of Medicare patients are Standard Eligible beneficiaries. If you then examine the phase of coverage for those patients, you see that 72% of consumption is occurring in the Catastrophic phase of coverage. The combination of these two metrics then demonstrates that approximately 18% of Enbrel Medicare patients could benefit from a $2,000 out-of-pocket cap (72% x 25%).

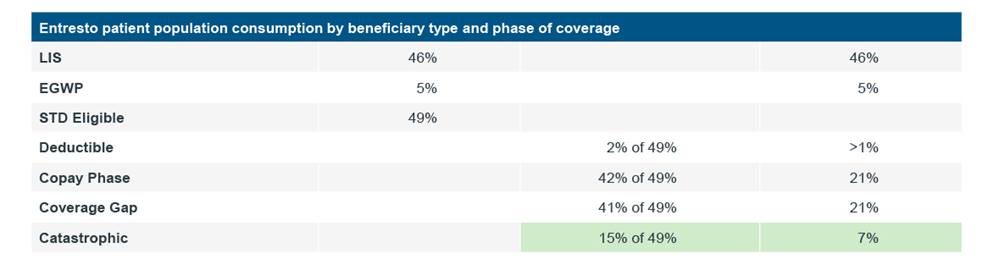

In another example, if we look at the impact on Entresto for patient copays, we see that the current list price is $668. With a new Maximum Fair Price of a 25% discount based upon the time on market, that gives us an MFP reference price of $501 ($668 x (1-25%)). Using an actuarial-driven copay of 25% off the new MFP price, that would place the beneficiary copay at $125. Patients currently pay less than that under the existing benefit design based upon Novartis’s contracted positions and the plans’ fixed copays. That means that 93% of Medicare patients on Entresto will not see material changes in their out-of-pocket expenses from the current benefit design. Of those that do, concentrated in the Catastrophic phase, they will experience approximately a $33 decline in copay per month.

Novolog represents a special case, as other provisions of the IRA cap insulin copays at no more than $35. As such, additional regulations will limit patient out-of-pocket exposure. For those patients who do consume insulin in the Catastrophic phase of coverage under the new benefit design, they will see a reduction in copay to $0.

The Inflation Reduction Act will impact many stakeholders as economics shift. The vast majority of patients, many who struggle with limited choice and affordability challenges, will experience little if any economic relief. Well-intentioned spend capitations will help seniors who consume drugs in the Catastrophic phase, but system savings from Maximum Fair Price negotiations will have little impact on out-of-pocket costs.

At the time of publication, multiple lawsuits from the industry are pending in attempts to block all or pieces of the legislation from going into effect. For this blog, we will assume that the law is implemented as passed.

Special thanks to Marcella Vokey, Ingrid Hirt, Jeanna Haw, James Brown, Rob Glik, Jeff Thiesen, Michael Kleinrock, and Mason Tenaglia for their contributions.

Read the next chapter in the Inflation Reduction Act Series

Part 4 of this 5-part blog series will explore how the IRA will affect competition. While these changes are intended to reduce drug prices and spur innovation, might the opposite prove true? Read the story.

Related solutions

Data, AI, and expertise empower Commercial Solutions to optimize strategy, accelerate market access, and maximize brand performance.

Gain high value access and increase the profitability of your brands