In December 2025, the IQVIA Institute for Human Data Science released Digital Health Trends 2025: Business Models, Evidence Requirements, and Revenue Opportunities, our sixth report examining the evolution of digital health. Since our first analysis in 2013, the sector has grown from simple wellness apps to sophisticated platforms and care solutions integrating digital therapeutics, biometric sensors, and AI-driven analytics.

Today, developers face mounting pressure to not only survive but to lead in the market by delivering solutions that outperform competitors on scope and breadth, evidence of cost effectiveness, care integration, and user experience. To overcome adoption barriers and avoid the commercial pitfalls faced by early entrants such as Pear Therapeutics, leading developers are deploying creative strategies to demonstrate value in an increasingly competitive landscape.

This year’s report explores how developers are competing and succeeding by diversifying their business models, acquiring other companies to expand their offerings, and adding advanced features to differentiate their solutions. These moves will shape the next phase of digital health innovation as we enter 2026, as developers seek to make their digital solutions stand out from competitors and meet shifting stakeholder priorities — from payers demanding cost-effectiveness to providers seeking seamless workflows.

Trends in digital health business models

How are developers building the best digital health solution in the market? What characteristics are increasing the likelihood of adoption by other stakeholders? Here are eight strategies developers are using to build best-in-class solutions and outpace rivals.1

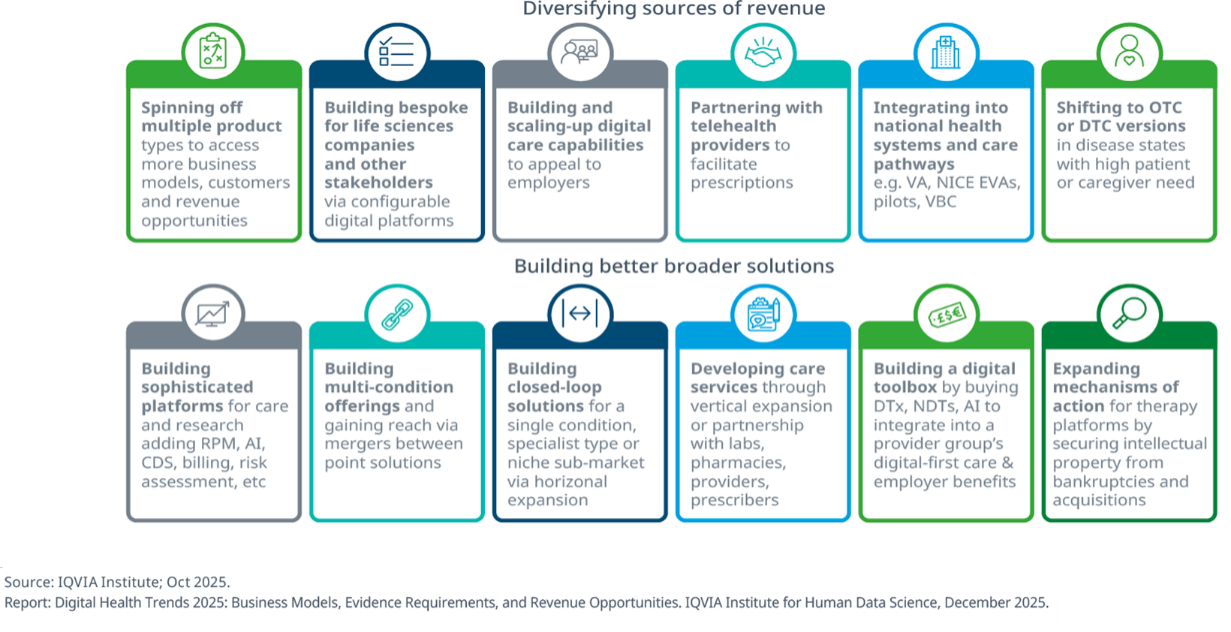

- Diversifying offerings and business models — spinning off solutions for new customers

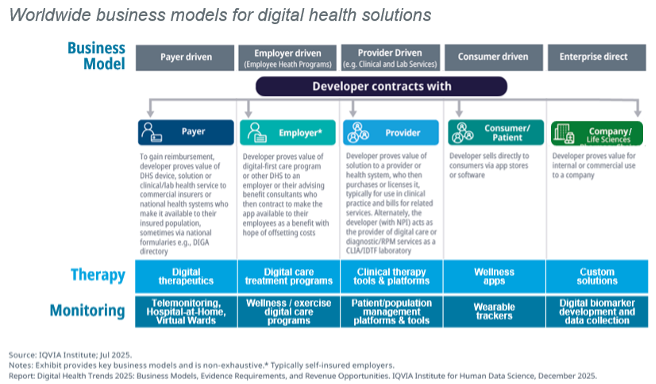

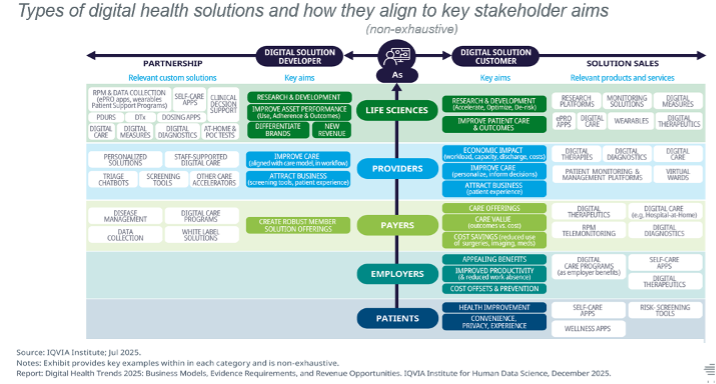

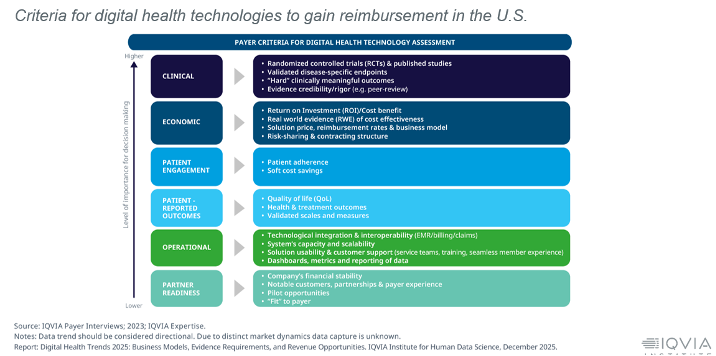

With commercial opportunities inconsistent across markets and a fragmented payer landscape in the United States limiting reimbursement, developers have been diversifying their business models. Rather than focusing on a single product type, they are spinning out differentiated offerings for consumers, employers, providers, payers, and life sciences partners to diversify their revenue. By doing so, they reduce dependency on any single customer and extend their reach.

For example, building on a therapeutics platform, leading developers may now simultaneously offer:

- Wellness apps with self guided content (for consumer purchase on app stores)

- Digital therapeutics (for prescribing and payer reimbursement)

- Clinical therapy platforms and tools that enhance care (for health systems and providers to license)

- Digital care treatment programs with coach or provider support (for health plans to offer employers as wellness benefits), and

- Custom “white-label” therapeutic solutions (for life sciences partners and other enterprises to use or market as their own solutions)

Likewise, in the remote monitoring space, developers are pairing their sensor-based devices and wearables with patient management platforms to better serve providers; clinical research platforms to support data collection and development of digital biomarkers by life sciences companies; and hospital-at-home care delivery models.

Ultimately, by addressing multiple market segments, developers are finding more paths to revenue and commercial success that can help sustain and expand their business.

-

Building stepped-care solutions that adapt to a patient’s needs across their care journey

Companies are now building digital health ecosystems that support stepped‑care — where patients can be moved flexibly between different levels of care based on need. They do so by combining various types of digital health tools with provider support. For instance, a single care platform may use AI‑based decision‑support or screening tools to help triage patients, wellness apps for patients to use for self‑management, prescription‑grade digital therapeutics to treat conditions, and wearables or ePROs to remotely monitor progress and inform care-plan changes.

Many of these solutions also support individuals end‑to‑end across their care journey — from prevention to diagnosis and treatment, through to monitoring and maintenance phases of therapy— creating patient experiences that feel continuous rather than fragmented.

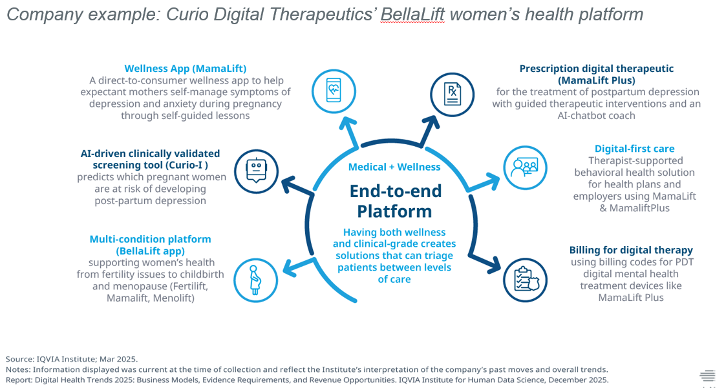

One example is Curio Digital Therapeutics’ Women’s Health platform which, as discussed in the 2025 Institute report on this topic, addresses several conditions including fertility, pregnancy, and menopause, and exemplifies this trend of assembling digital toolkits to screen, treat, and monitor patients in a single stepped care model (shown below).1 Within this therapist‑supported ecosystem, an embedded AI‑driven screening and risk‑stratification tool, Curio‑I, helps providers to identify women at risk for postpartum depression and route them to the appropriate level of support — such as self‑care for wellness or prescription digital therapeutic intervention.

By offering personalized, flexible care stepped care models to match patients to the right level of support, companies position themselves as cost effective options for populations with varying needs — appealing to employers, health plans, and insurers. The use of varied digital health product types within care also creates opportunities for digital care providers to benefit from new reimbursement opportunities that may emerge —including, for Curio, new billing codes established for FDA‑cleared digital mental health treatment devices under the 2025 Medicare Physician Fee Schedule.

- Repurposing platform technologies to launch products more rapidly

Much like biopharma applies proven drug delivery technologies to new medicines, digital health developers have been repurposing their core software platforms to deliver a broader array of solutions. Instead of building each product from scratch, they are leveraging pre existing platform infrastructure — including analytics engines, algorithms, content libraries, user interfaces, AI driven personalization tools, and integrations that collect data from sensors and wearables —and adapting their polished software modules for new use cases. Such functional modules may support diverse functions, from guiding therapy using validated mechanisms of action, to enabling billing, patient education, remote monitoring and population health. By reusing this proven infrastructure, teams can rapidly create new offerings in adjacent therapeutic areas or adapt their solutions for new customer segments.

“Click Therapeutics describes itself as having “shared platform technologies with novel cognitive, behavioral and neuromodulatory mechanisms of action” and Mahalo Health positions its platform as having “digital therapy building blocks” that snap together like Legos to create digital companions.” 1,2,3

This strategy is already visible in the market: leveraging their platforms, Sidekick Health (and others) co develop digital therapeutics with life sciences companies; Welldoc and Glooko produce white label chronic disease apps for health systems; and Germany’s DiGA developers, including HelloBetter and Selfapy, have expanded their portfolios by applying similar psychotherapeutic approaches and modules across multiple mental health conditions. 4,5,7

An analysis by IQVIA Digital Health suggests that this platform based approach may be shortening development timelines and helping digital health companies introduce new products more rapidly. Their findings, highlighted in the report, show that second generation DiGA products reached the market within two to three years—far faster than the seven to ten year timelines that characterized early market entrants. The reduced technical burden and efficiency gained by building on established platforms helps mature developers to position themselves as flexible partners able to deliver customized solutions for diverse stakeholders and meet their needs.

-

Consolidating to build the best and broadest clinical platform in their segment

Digital health companies have been acquiring one another and merging to broaden the therapeutic scope of their solutions and the range of mechanisms they can deliver. Some digital health companies are building leading platforms in specialized technology niches — such as extended reality (XR) or serious games — while others are building platforms that serve specific provider types and specialties, like neurologists or oncologists.

XRHealth exemplifies this trend in the virtual and extended reality (VR/XR) space. Between 2023 and 2025, through a series of mergers and acquisitions (including Amelia Virtual Care, NeuroReality, RealizedCare and Innerworld) the company assembled a suite of immersive tools to create one of the largest XR focused health platforms globally.1,7 The platform spans multiple conditions — relating to cognition, behavioral health, pain management, and physical and neurological rehabilitation — and the company laid the groundwork for more personalized care with its acquisition of a triage tool and patenting an AI‑enabled biofeedback system that would adjust treatment based on biometric and motion data, such as from wearables.

As a result, the company can now license its leading XR therapy platform to diverse healthcare providers, deliver clinician led telehealth supported by immersive VR, and run home based wellness programs for stress, pain, and mental health that appeal to employers, health plans and consumers. With the creation of a new a billing code E1905 by Centers for Medicare & Medicaid Services (CMS) in 2025, its virtual reality headset that delivers cognitive behavioral therapy (CBT) can now also reimbursed by Medicare as Durable Medical Equipment (DME).8,9 Such acquisition‑driven growth has not only become one of the most direct paths for developers to assemble a pre‑eminent platform ecosystem within a specific product segment and strengthen their market position — but also to increase their appeal with diverse stakeholders and unlock multiple revenue streams.

-

Incorporating AI to deliver timely and personalized care — novel now, but soon a necessity

Artificial intelligence is rapidly becoming a foundational backbone of modern digital health platforms — and a key element of competitive advantage. Both in the remote monitoring and digital therapy space, leading companies now integrate AI throughout their platforms and across the entire care journey – setting a new bar for the clinical value digital health technologies can provide.

They incorporate multiple AI‑driven functions to enable earlier intervention, personalize and optimize decision‑making, and improve operational efficiency — aiming to ensure their solutions meet the needs of various health stakeholders: payers seeking to reduce avoidable utilization and costs; employers seeking personalized support for diverse employee needs; and health systems hoping to extend provider capacity with tools that ease administrative burden and anticipate clinical needs.

For instance, AI‑enabled decision support and predictive analytics help providers identify high‑risk patients, triage them to appropriate levels of care, optimize care plans, and anticipate clinical deterioration to intervene earlier. At the same time, AI built into apps can simply enhance the patient experience by acting as chatbot guides to help patients navigate content.

Together, these AI enabled capabilities are elevating digital solutions from supportive tools to essential components of modern care delivery. By making predictive intelligence a core feature, digital health companies are transforming their platforms into strategic assets for health systems operating in increasingly complex care environments —differentiating themselves from competitors that offer only passive data dashboards. As digital health adoption accelerates, AI‑powered insights are likely to shift from optional to expected features.

-

Expanding therapeutic focus to deliver multi condition care and make life easier for purchasers

Responding to a shift in purchaser preference to contract with digital care companies whose solutions address multiple conditions, digital care providers are expanding the therapeutic focus of their platforms. According to the Peterson Health Technology Institute, in the U.S., 92% of employers, 88% of health systems, and 81% of health plans reported that covering a wide range of clinical indications was important to them when evaluating digital health offerings —likely driven by the desire to simplify procurement, reduce vendor fragmentation, and deliver value across diverse populations.10 These considerations may be especially important to payers and health plans offering digital health solutions and formularies to the employer market.

To meet this shift, digital solution providers are expanding their platforms to address a broader range of conditions. DarioHealth, for example, evolved from a diabetes‑focused offering to a multi‑condition platform by expanding into musculoskeletal and behavioral health through its 2021–22 acquisitions of Upright Technologies, wayForward, and Physimax.1,11,12 It then further extended its virtual care capabilities into maternal and mental health with the acquisition of Twill in 2024.

As purchasers favor contracts with fewer, more capable partners, building multi condition comprehensive care ecosystems is becoming increasingly essential to compete in a maturing digital health market.

-

Delivering “digital‑first” blended care to improve outcomes and adoption

Blended care models that combine digital health technologies with human support continue to grow in importance. Evidence that blended care can sustain engagement, adherence, and clinical benefit better over time as compared with standalone digital therapeutics have led companies to increasingly embed virtual care and telehealth services around their products.1,13

Our report discusses the various strategies developers employ to incorporate support from coaches, therapists, nurse navigators, and other clinical personnel. Some companies are building in‑house virtual care capabilities — becoming provider organizations and obtaining NPIs to bill for clinical services — while others partner with external telehealth groups to manage prescribing, coaching, or clinical oversight. Still others use management services organization (MSO) or platform‑licensing models to support networks of affiliated but independent providers.

In this evolving market where provider awareness of digital health technologies remains limited, these approaches also streamline patient access and reduce friction for traditional clinicians — who would otherwise need to incorporate unfamiliar digital tools into already burdened workflows — and help companies meet evolving payer reimbursement requirements for clinician involvement in care planning and outcomes monitoring.

-

Prioritizing interoperability and health system integration capabilities — now a driver of category leadership

Finally, adoption remains a key hurdle. Providers want solutions that reduce work, not add to it, and health systems increasingly expect digital platforms to minimize administrative burden, align with established care pathways, and fit naturally into existing clinical infrastructure. For developers, this means that category leadership now hinges on their technological and operational ability to integrate solutions into care settings.

To meet these expectations, developers are building their integration capabilities and making their solutions workflow-friendly. They are building their platforms to be interoperable and capable of data exchange with EHRs (increasingly via SMART on FHIR) — so information flows directly into patient records without manual entry — to seamlessly align with existing clinical and administrative workflows, and support prescribing, documentation for claims, and reimbursement processes.

As staffing shortages persist and provider capacity tightens, developers that make integration effortless for health systems and reduce provider workload are likely to become preferred partners and can claim a decisive competitive advantage, whereas competitors that overlook these operational essentials risk being sidelined by health systems.

Looking Ahead

The race for leadership in digital health is gaining momentum. As competition intensifies, developers will continue to innovate to lead their specific product segments and shape the future of care delivery. This year’s analysis points to an industry moving beyond early experimentation and toward more mature solutions that can meet the rising evidence requirements and expectations of payers, employers, providers, and health systems. The IQVIA Institute for Human Data Science will continue to follow the development of digital health and AI technologies, and how they are changing care, drug development, and R&D.

1 Unless noted, all information is sourced from IQVIA Institute for Human Data Science. Digital Health Trends 2025: Business Models, Evidence Requirements, and Revenue Opportunities. December 2025.

2 Otsuka. Otsuka and Click Therapeutics announce the U.S. Food and Drug Administration (FDA) clearance of Rejoyn, the first prescription digital therapeutic authorized for the adjunctive treatment of major depressive disorder (MDD) symptoms [Internet]. 2024 Apr 1 [cited 2026 Mar 2]. Available from: https://otsuka-us.com/news/rejoyn-fda-authorized

3 Mahalo Health. Rapid Digital Therapeutics (DTx) Development Platform. Accessed 2025 Jan 24. Available from: https://www.mahalo.health/products/digital-therapeutics-development-platform

4 Welldoc. One platform Connecting individuals, care teams and health organizations. Accessed 2024 Feb. Available from: https://www.welldoc.com/solutions/chronic-care-management-platform/

5 Glooko. Glooko Clinical Research. [Accessed 2024 Feb 6]. Available from: https://glooko.com/clinical-research-products/

6 HelloBetter. DiGA examples: The building blocks of a digital health application at a glance. Available from: https://hellobetter.de/aerzte-psychotherapeuten/diga-beispiele/. 11/22/2024 and Digitale Gesundheitsanwendung (DiGA) verordnen | HelloBetter Available from: https://hellobetter.de/diga-verordnen/ [Accessed Feb 24, 2026]

7 XRHealth. Press Releases [Accessed Feb 24, 2026]. Available from: https://www.xr.health/us/press/

8 XRHealth. XRHealth Homepage: AI-powered extended reality [Internet]. 2026 [cited 2026 Mar 2]. Available from: https://www.xr.health/

9 XRHealth. How VR CBT Devices Are Now Covered as DME: What Patients Need to Know. 2025 May 7. Available from https://www.xr.health/us/blog/how-vr-cbt-devices-are-now-covered-as-dme-what-patients-need-to-know/

10 Peterson Health Technology Institute. 2024 State of Digital Health Purchasing. 2024 Mar. Available from: https://phti.org/wpcontent/uploads/sites/3/2024/10/PHTI-2024-State-of-Digital-Health-Purchasing-Survey.pdf

11 DarioHealth. DarioHealth newsroom [Internet]. Available from: https://www.dariohealth.com/newsroom/ [cited 2026 Mar 2].

12 DarioHealth. DarioHealth enters agreement to acquire Physimax [Internet]. 2022 Jan 20. Available from: https://dariohealth.investorroom.com/2022-01-20-DarioHealth-Enters-Agreement-to-Acquire-Physimax,-a-Leading-Provider-of-Validated-Computer-Vision-for-Musculoskeletal-Health

13 Peterson Health Technology Institute Health Technology Assessments, 2024 through-mid 2025. Available from: https://phti.org