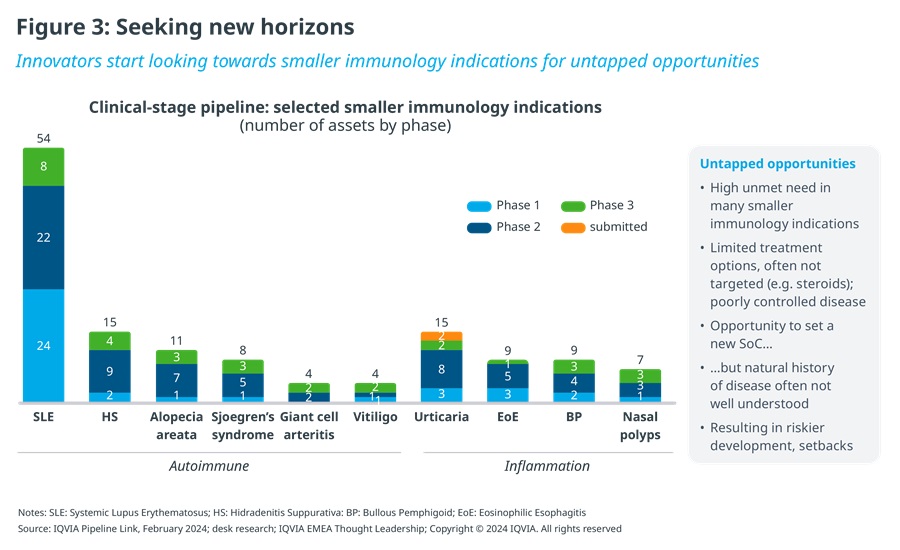

Unmet need is high in a long list of largely neglected immunological diseases, such as systemic lupus erythematosus, hidradenitis suppurativa, alopecia areata, Sjögren's syndrome, vitiligo, bullous pemphigoid or prurigo nodularis. Their prevalence spans a range from rare diseases with fewer than 200 thousand patients in the US, for example, to relatively more common conditions with a million or more patients, a subset of whom are severe cases most in need of innovative therapies. What they share is having been underserved, with typically limited disease-specific treatment options available to date, leaving many patients with poorly controlled disease. This represents an attractive opportunity for innovators to set an effective, new standard of care.

However, the natural history of these diseases is often less well understood and has led to several setbacks, e.g., in lupus. Nevertheless, innovators are clearly not disheartened, judging by recent pipeline momentum. For example, hidradenitis suppurativa has seen a major inflection point in development activity after many years of an innovation drought and was a key focus at the recent annual meeting of the American Academy of Dermatology (AAD), with several high-profile presentations of mid- to late-stage readouts, including AbbVie’s IL-1α/1β antagonist lutikizumab, Novartis’ oral BTK inhibitor remibrutinib, and Moonlake’s anti-IL-17 nanobody solenokimab.

The overall change in innovation intensity that we are witnessing across underserved immunology diseases is reminiscent of the momentum that transformed today’s major autoimmune indications about 10-15 years ago. However, without such epidemiological scale, innovators today must play across multiple of those smaller indications to achieve critical mass in an immunology franchise, e.g., via a portfolio of assets and/or multi-indication assets.

Seizing the opportunity

Finding success in less explored immunology indications requires a different approach. Unlike the major, well-established autoimmune conditions such as RA, psoriasis or Crohn’s disease, smaller indications face unique challenges, for example, often low disease awareness among patients and HCPs, a limited understanding of the burden of illness and its true impact on patients’ life, immature care pathways, including diagnosis, specialist referral and treatment, leading to under-diagnosis and under-treatment, or convincing payers of the need to treat and for them to cover novel therapies.

Innovators targeting smaller, oft neglected immunology indications therefore must focus on three priorities:

- Patient-relevant evidence, going beyond traditional endpoints used in immunology to assess true patient impact, including QoL. For example, we have seen recent efforts in defining clinically more meaningful and patient-relevant composite endpoints for Sjögren's syndrome, e.g., CRESS (Composite of Relevant Endpoints for Sjögren's Syndrome), combining 5 complementary measures that collectively better capture disease severity to assess treatment response and patient outcomes, given the heterogeneous and complex nature of primary Sjögren's syndrome. Partnering with medical societies and opinion leaders is critical for validation and acceptance of novel endpoints.

- Close collaboration with patient advocacy groups, for example to gain input from patients in defining patient-relevant endpoints, help with patient recruitment for clinical trials, support disease awareness building or as patient advocates in efforts to secure market access and reimbursement for novel therapies.

- Extensive market shaping and health system preparation, focussing on raising awareness of the disease, unmet need and its patient burden; building advocacy for the need to treat with innovative therapies and shaping treatment guidelines; and facilitating health system readiness, e.g., establishing or streamlining care pathways, or embedding new diagnostic tools and standards. This requires early, external engagement, especially medical affairs-led, and the deployment of dedicated roles focussed on health system enablement.

As innovators re-direct their efforts towards historically underserved immunological diseases, long-suffering patients will be the ultimate winners, as the prospect of effective treatment options makes big strides towards becoming reality.