Biogen in pole position

It is coming up to six months since the launch of four Humira (adalimumab) biosimilars in Europe, and their manufacturers have since been tussling to capture share from the originator. IQVIA has compiled data to January 2019 and with it, we can explore little over three months of the forces at work.

Tender results and early switch analyses had indicated that Imraldi, the biosimilar created by Samsung Bioepis and marketed by Biogen, had the upper hand in the largest markets by molecule usage: the UK and Germany.

You can click here to read my first article which elaborates further on the early dynamics of Humira biosimilars.

Slower launch than previous biosimilars

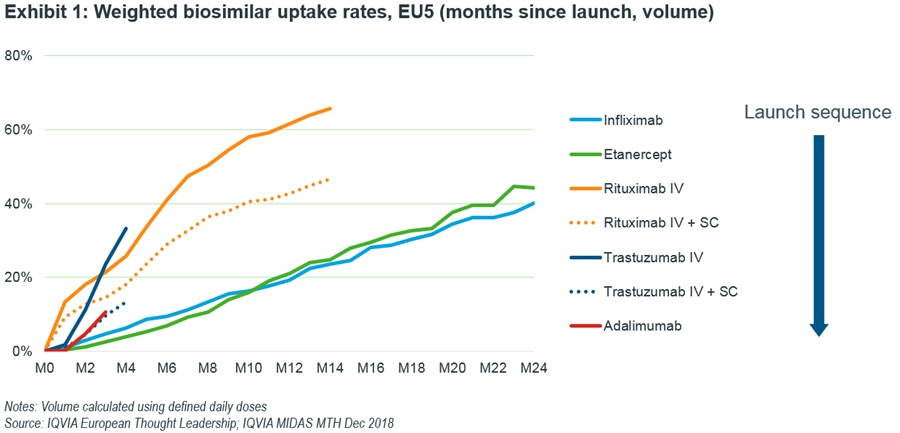

The last few biosimilar entries (infliximab, etanercept, rituximab and trastuzumab) have shown a general trend, in that the most recent launches had faster uptake rates than the previous ones. This also holds true when considering the protected subcutaneous versions of rituximab and trastuzumab.

However, adalimumab has broken this trend. As of December 2018, the aggregate uptake of adalimumab biosimilars in EU5 countries (UK, Germany, France, Italy and Spain) was slower than that of trastuzumab and rituximab which is suggestive of AbbVie’s willingness to negotiate assertively in order to protect market share (Exhibit 1).

Further analysis at the country level reveals a contrasting picture. While Germany and, to a lesser extent, the UK are tracking at the same rate as previous launches, it is Italy, France and Spain that are lagging. In France, reasons include reduced incentives for community pharmacists to distribute biosimilars and in England, the contract came into effect in December, so volume uptake should pick up pace going forward).

Imraldi inches ahead

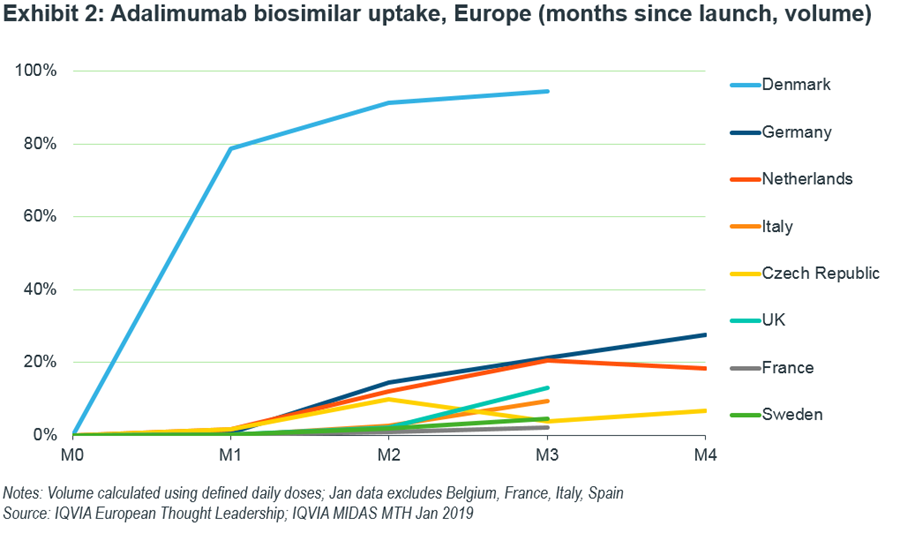

Denmark, with its winner-takes-all tender, has switched nearly all patients to the biosimilar with 80% uptake in the first month by volume. As such, it leads in terms of uptake.

Germany is currently tracking faster than the UK which is unusual as the UK’s typical uptake pattern is normally steeper (Exhibit 2). Again, this could change as contracts came into effect in December. France, Italy and Spain are hovering below 10% uptake.

The absence of Norway is notable as it is commonly a fast country; it has not launched a biosimilar as AbbVie won this country’s tender.

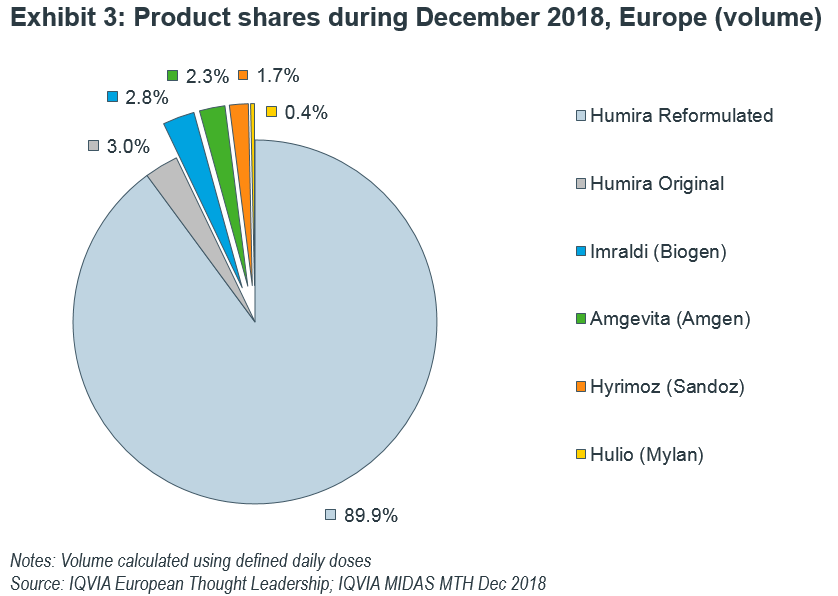

Across all European launches of adalimumab biosimilars, Imraldi is in top position having captured 2.8% of total molecule volume as of December 2018, but followed closely by Amgevita and Hyrimoz with each under 3% of total volume (Exhibit 3).

Country-level dynamics reveals a nuanced picture

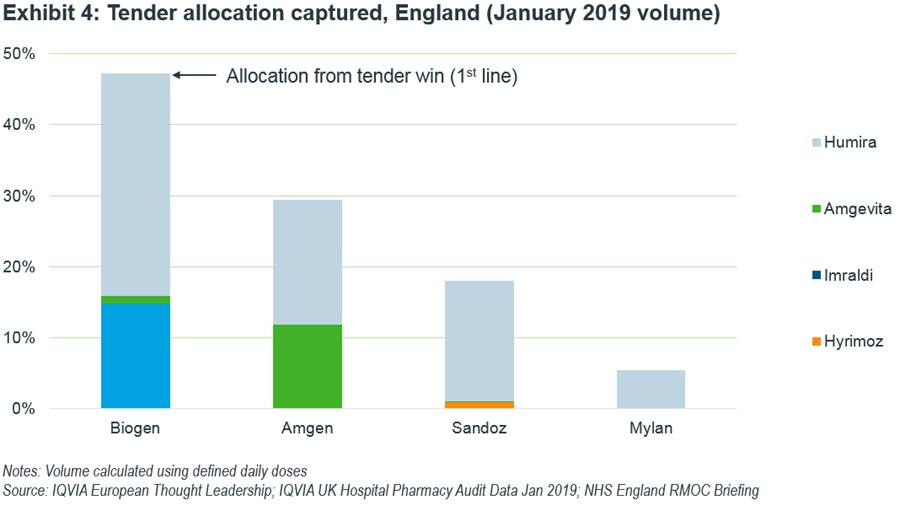

Within England, some interesting uptake dynamics between competitors come to light. In my previous article, I calculated the potential shares accessible to each product using the regions allocated to each manufacturer won from the national tender as 1st line therapy. Now, with January 2019 data available, we can observe actual volume captured (Exhibit 4).

Samsung and Biogen have indeed been successful in gaining share, while Sandoz, surprising compared to their performance in Germany, which is lagging in capturing patients with Hyrimoz. Mylan/Fujifilm Kyowa Kirin are yet to gain traction in their tender-allocated regions.

Amgevita is closest to taking half of its allocated region share and has gained further ground in encroaching into Biogen’s regions. This is most likely as it was awarded second line thanks to its improved formulation intended to reduce injection site pain.

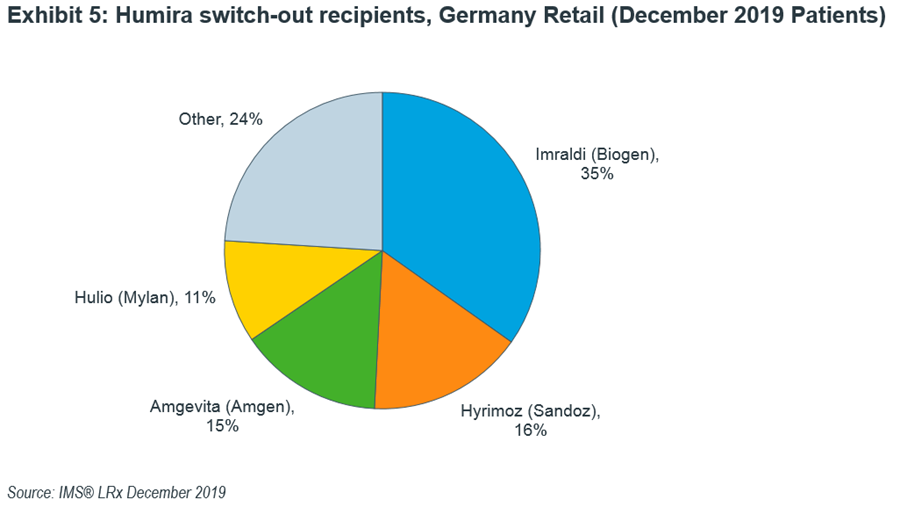

Patient level data in Germany’s retail channel (where the majority of Humira is dispensed) shows that Imraldi tops the Humira patient switch-outs as was the case in November 2018. Again, Hyrimoz and Amgevita took second and third spots but fastest gainer is Mylan’s Hulio with 11% wins in December, up from 2% in the previous month (Exhibit 5).

Moreover, switching is not unidirectional either. In December, Humira lost 35% of patients to Imraldi but gained 1% in switchbacks giving a net total of 34% losses to Imraldi. This could be due to Humira’s improved formulation coupled with the patient/physician familiarity with the originator product.

Three key take-aways

After one hundred days of Humira biosimilars on the market, we can observe a few notable trends:

- Slower than anticipated uptake: Overall uptake in European markets compared to previous launches seems to be shallower, potentially due to competitive discounting from AbbVie (in its Q3 2018 investor transcript, AbbVie’s CEO stated that discounts had been “on the higher end of planning scenarios”).

- Patient centricity matters: In England, 2nd line winner Amgevita has gained additional market share due to its improved formulation. This shows that patient convenience is a deciding factor for physicians and can override economic incentives.

- Switches are not unidirectional: Switches back to Humira are already seen in Germany. Again, this could be a reflection of Humira’s improved formulation compared to Imraldi as a driving force for this.

Humira’s improved formulation has not used patents to keep out biosimilar copies, but it has added a prescribing incentive for physicians that see its benefit. Evidence shows that switchbacks to Humira and 2nd line progression to biosimilars with this improved formulation have already begun.

All players should monitor these switches closely to understand how their share of the market will evolve.

For more information on biosimilars, please reach out to me via email.

- To read more on Humira Biosimilars, click here.

- To understand the Oncology Biosimilars market, click here.