To date, key factors in the 2023 U.S. pharmaceutical market include the fact that biologics continue to grow at a higher pace than non-biologics (with specialty drugs1 accounting for more than half of the total market) while revenues from unbranded generics continue to decrease despite rising prescription rates. These elements were topics of discussion at IQVIA’s virtual conference, Fusion 2023: Intelligently connecting data, tech, and analytics, held on May 16-17, 2023. The conference was designed to enable participants to imagine the next steps in optimizing complex and comprehensive datasets, within the right technologies, to generate more accurate and more repeatable insights.

Declining incidence of COVID-19, coughs, colds, influenza, and RSV

Participants at Fusion 2023 heard that COVID-19-related deaths continue to fall, along with incidence of RSV, cough, colds, and influenza. Deaths from COVID-19 have diminished to close to levels very early in the pandemic, an indication that at least for the present, this is becoming less of a threat. In line with this trend, COVID-19 vaccine uptake continues to diminish, from around 6% of prescriptions in 2021, to 2.5% in 2022, and less than 1% in 2023. Significant spikes were seen in both RSV and norovirus during the latest U.S. cough, cold and flu season, with RSV incidence increasing sharply in the fall of 2022 and continuing into early 2023.

Interestingly, the Australian flu season in mid-2022 and the U.S. flu season in winter 2022-23 both peaked earlier than seasonal averages and experienced only one significant peak. In both countries, pediatric patients saw a particularly high incidence of flu, potentially due to reduced immunity following lack of exposure to others during the pandemic..

Specialty drug growth outpaces traditional drugs

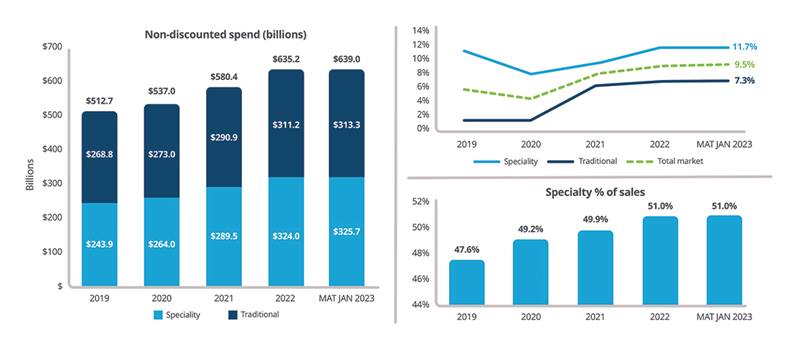

In 2022, specialty product growth outpaced traditional product growth, with a 51% share of total non-discounted spend (Figure 1). In the moving annual total (MAT) to January 2023 (MAT January 2023), specialty spend grew by 11.7% while traditional growth grew 7.3% on an invoice price basis.

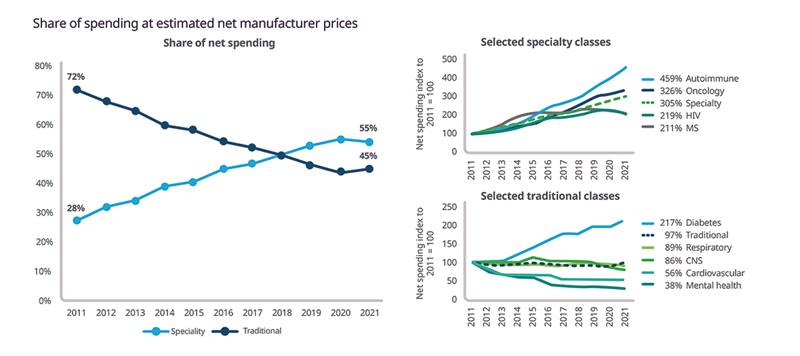

As of March 2022, specialty medicines accounted for 55% of net spending, up from 28% in 2011. This increase was driven by growth in the autoimmune and oncology sectors (Figure 2).

Figure 2: Share of spending at estimated net manufacturer prices

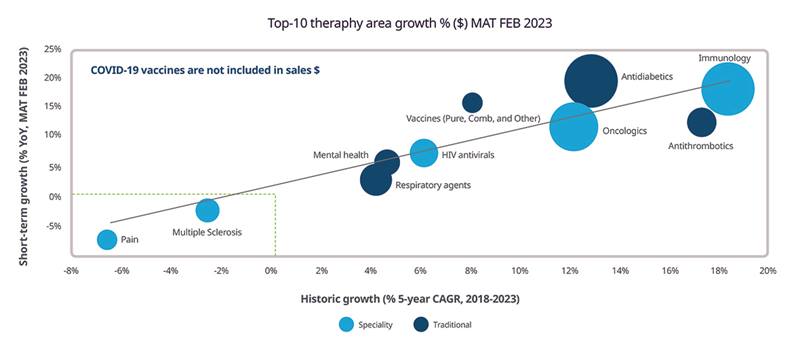

Immunology and antithrombotics currently lead short- and long-term sales growth, as illustrated in Figure 3.

Figure 3: Sales growth in top 10 therapy areas, February 20

Outlet dynamics: Retail pharmacy stores continue to close

Almost 700 pharmacies have closed in the U.S. retail sector over the last two years, with numbers of stores forecast to continue to decrease, including closures at CVS, Walgreens, and Rite Aid. Key events in this segment include Kroger’s and Albertson’s planned merger, and Amazon Pharmacy launching a service offering unlimited generic drug prescriptions for a flat fee of $5 per month. Reduced pharmacy store hours are also widespread due to retail pharmacy staffing issues.

Food store pharmacy sales (from grocery stores which contain pharmacies, such as Kroger’s, Albertson’s and Publix) recorded a compound annual growth rate (CAGR) of 5.9% in 2022, with mass market recording a 0.9% CAGR, and chain stores (such as Walgreens, Rite Aid and CVS) seeing an overall 0.2% decrease. This is in line with an overall trend for growth in retail to be driven by chain and food in recent years.

Medicare Part D sees largest volume growth among payment methods

Among methods of payment, Medicare Part D has consistently seen the largest volume growth over the last four years, from 33.7% market share in 2019 to 34.9% in 2022. Discount cards have seen the highest CAGR during this time, tied to availability of generics and biosimilars, with some slowing in growth from 2021 to 2022. Use of cash continues to decline. Third-party payments (from private health insurers and others) still have the largest market share, but are also diminishing, from 45.3% in 2019 to 42.9% in 2022. Medicare has grown from 12.6% to 13.6% of the market during that period.

Generics and biosimilars: Opportunities as more biologics lose exclusivity

In 2022, 87.2% of small molecule drug prescriptions were dispensed as unbranded generics (adjusted figure), while only 8.5% of revenues came from this category of products. The generic price trend remains near the midpoint of the historic ‘natural’ deflationary trend.

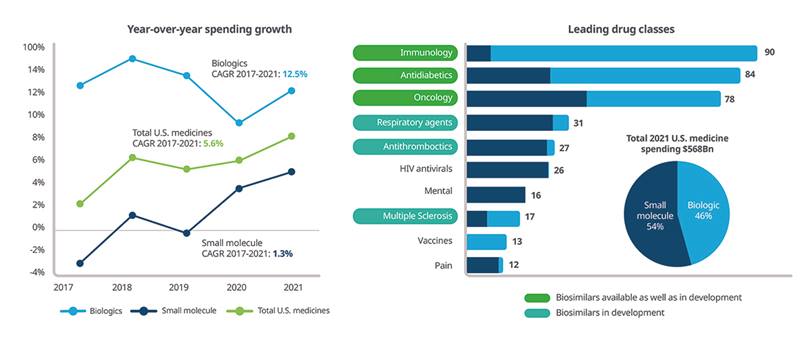

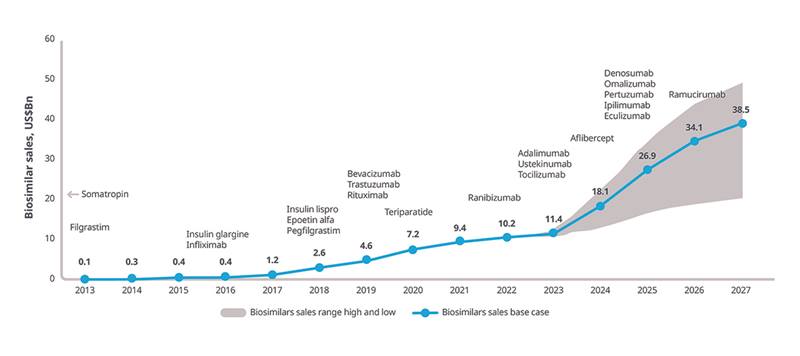

The biologics market continues to grow faster than non-biologics on an invoice basis, currently accounting for 46% of spending (Figure 4), or some $260 billion, of which 14% is accounted for by molecules facing biosimilar competition ($38 billion), and 70% is held by molecules with potential future biosimilars ($181 billion). Since 2007, 30 biosimilars have been launched in the U.S., with 10 more approved and set to launch by the end of 2023. In oncology, market shares held by biosimilars range from 66% to 84%.

Figure 4: Total U.S. invoice spending growth by type and leading therapy areas (2021 spending, $ billion)

The biosimilars market will continue to expand as losses of exclusivity occur, with expected launches and uptake forecast to increase overall spending on biosimilars to $20-49 billion in 2027 (Figure 5).

Figure 5: Biosimilar historical sales 2013–2022 and outlook scenarios 2023–2027 ($ billion)

Increasing availability of biosimilars have differing implications for various stakeholders. For example, for patients, insurance coverage and out-of-pocket costs are key factors. For payers, reimbursement decisions, and formulary placement of biosimilars will impact uptake, and interchangeability will need to be addressed. For providers, key factors include patient stability and compliance with current therapy, likelihood of payer coverage, and incentives for biosimilar prescribing. Biosimilar companies will need to identify viable opportunities for biosimilar development based on factors such as return on investment, and the cost vs. benefit of interchangeability.

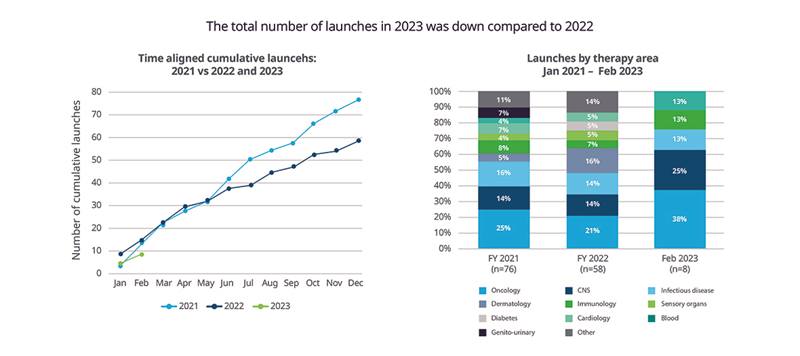

New launches: Oncology accounts for 38% of new products

There have been eight launches to date in 2023, compared to 11 launches for the same period in 2022, with oncology accounting for 38% of product launches in 2023. In 2023, four of the eight new molecular entities (NMEs) approved by the U.S. Food and Drug Administration (FDA) show evidence of launch based on supply in channels or active websites. In 2022, the FDA approved 36 NMEs, of which 33 show evidence of launch. Recent launches are illustrated in Figure 6.

Figure 6: Pharmaceutical product launches by therapeutic category in 2021-23

Conclusion: COVID-19 abates, specialty drugs dominate, and biosimilars promise growth

To date in 2023, trends in the U.S. pharmaceutical market include:

- COVID deaths and RSV, cough, colds, and flu are declining

- Specialty drugs currently represent around 51% of total market sales

- The role of the pharmacist is growing rapidly, with staff in short supply

- Pharmacy stores continue to close, with opening hours of remaining stores restricted due to pharmacy staffing issues. Food store pharmacies are seeing the highest CAGR growth

- Medicare Part D is recording the highest volume growth among payment methods, with a 34.9% market share in 2022

- Unbranded generics are growing in terms of prescriptions, accounting for 87.2% of prescriptions, but continue to fall in dollar terms, to only 8.5% of revenues

- Biologics account for almost half of drug spending (46%), growing faster than other products

- Biosimilars are now a reality, with Humira facing one U.S. competitor and many more expected. Most future loss-of-exclusivity opportunities will be in biosimilars

- So far in 2023, there eight new products have been launched, against 11 in the same period last year. Oncology accounts for 38% of launches

An understanding of these trends and how they will likely play out in future can support sponsors in successfully developing and modifying strategies for their commercial operations.

1 IQVIA defines specialty drugs as ones that meet these criteria:

- Treats chronic, rare, and/or complex diseases

- Initiated and maintained by a specialist

- Generally injectable and/or not self-administered

- Products that require an additional level of care in their chain of custody

- Expensive (USD $6K annual cost of therapy)

- Unique distribution

- Requires extensive or in-depth monitoring/patient counseling

- Requires reimbursement assistance

Top Trends to Watch in 2023

2023 is poised to be an important inflection point for much of healthcare in the United States: New strategies and technologies for educating and engaging healthcare providers, rising expectations, but stagnating engagement from patients, and a shifting legislative and regulatory landscape. What do we see on the horizon that you need to know? Tap into our 2023 trends below.

Related solutions

We empower life sciences with connected intelligence, transforming data into actionable insights for smarter decisions and better patient outcomes.