Financial Institutions

Maximize your healthcare investments, with evidence.

In our first blog of 2024 on biopharma M&A trends, we will provide an outlook for the year ahead, following a brief recap of how 2023 played out.

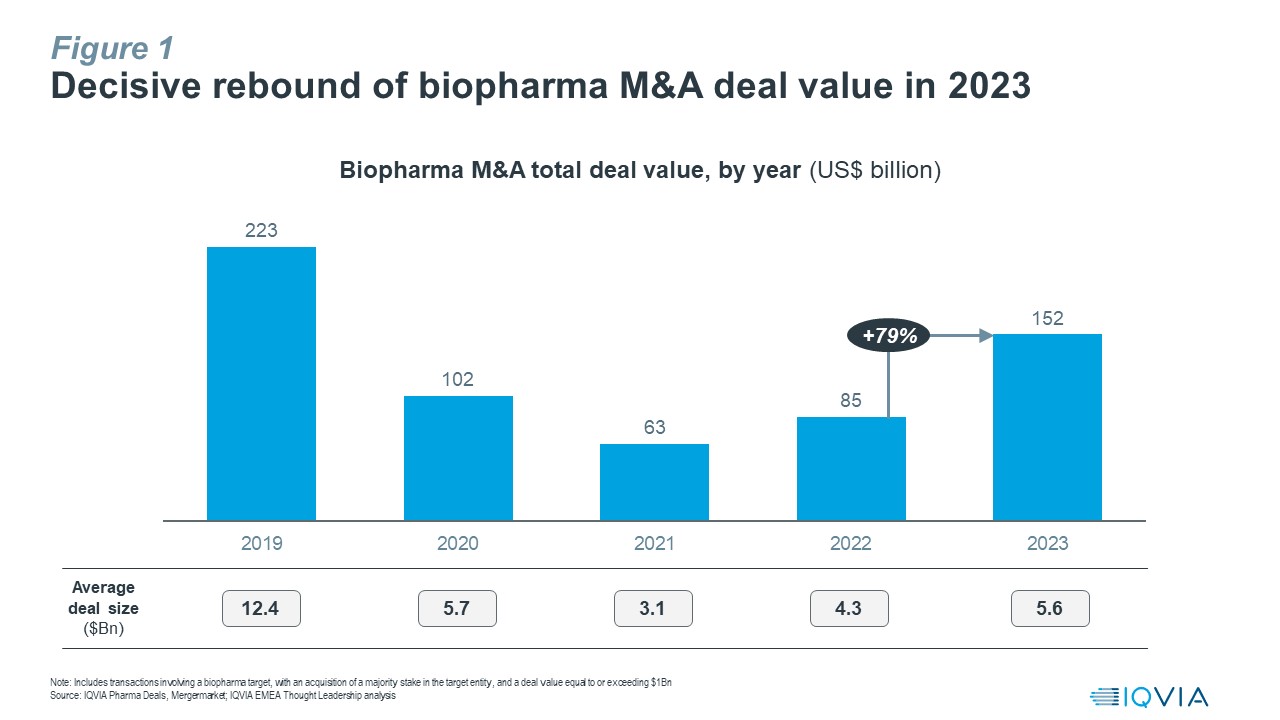

Biopharma M&A activity has witnessed a decisive rebound in 2023, with aggregate deal value up by 79% vs. 2022 to reach ~$152Bn for the full year, the highest since 2019. Average deal size also continued its upward trend towards levels last seen in 2020 (see Figure 1).

This outcome is in line with our prediction that we made early last year of M&A value in 2023 hitting a total of $140-160Bn for transactions involving a biopharma target, with an acquisition of a majority stake in the target entity, and a deal value equal to or exceeding $1Bn.

In 2023, bolt-on deals dominated, with the exception of the $43Bn Pfizer-Seagen acquisition as the only mega-deal announced last year. Noteworthy, sizeable transactions announced in 2023 include BMS-Karuna ($14Bn), Merck-Prometheus ($10.2Bn), AbbVie-Immunogen ($10.1Bn), AbbVie-Cerevel ($8.7Bn), Biogen-Reata ($7.3Bn) and Roche-Telavant ($7.1Bn).

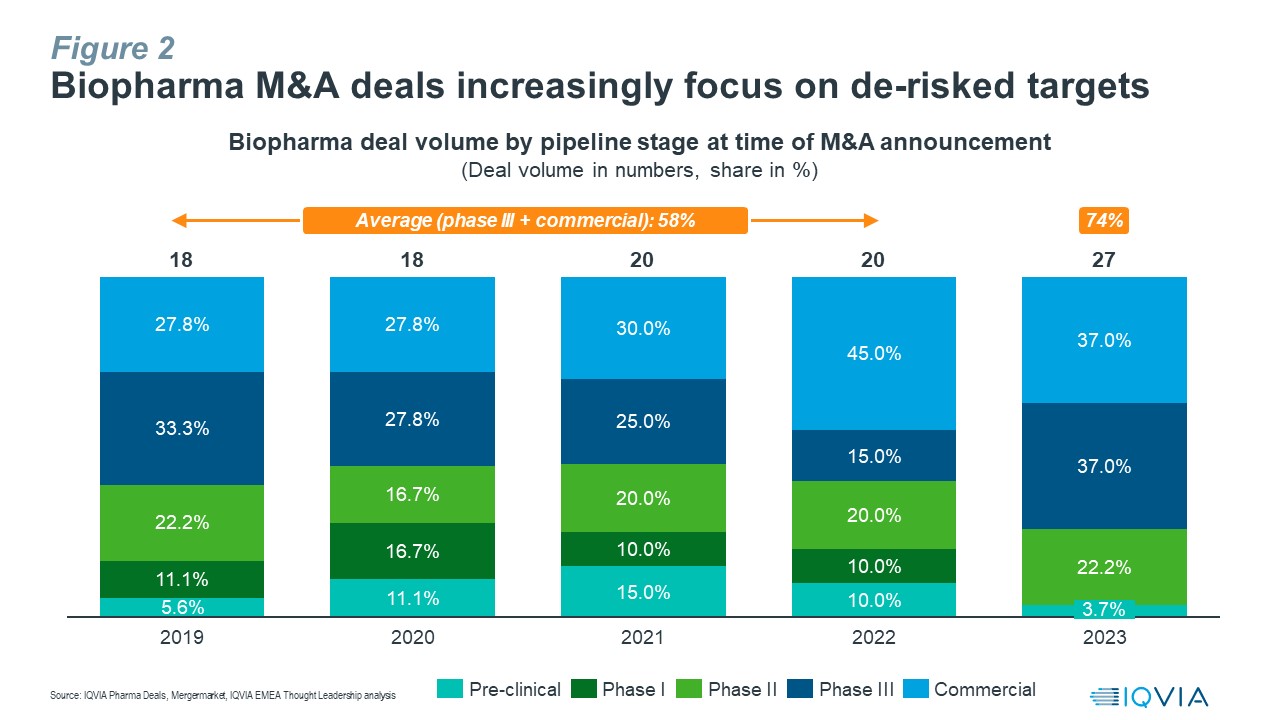

M&A deal activity in 2023 also highlighted a significant decline in acquirers’ risk appetite compared to previous years, with 74% of transactions focused on de-risked targets with assets which were at least in phase 3 or already on the market, an increase of 16% compared to the average share of 58% for such deals during the four-year period from 2019 to 2022 (see Figure 2).

Unsurprisingly, oncology as hotbed of biopharma innovation was the leading therapy area (TA) for M&A deals in 2023, representing 48% of deal value.

Interestingly, CNS, long shunned by big pharma, was the focus of several high-profile deals in 2023: BMS-Karuna ($14Bn); AbbVie-Cerevel ($8.7Bn) and Biogen-Reata ($7.3Bn), with the former two deals centred on leading schizophrenia assets with a novel MoA, muscarinic receptor agonists, for treating psychosis. Overall, CNS became the #2 TA in focus of M&A deals last year, with 21% value share.

Immunology dropped from its #1 spot in 2022 to third rank by deal value, with a share of 14%.

Cardiometabolic assets, especially those focussed on obesity, saw a surge in interest in 2023 as acquirers were eager to participate in the industry’s latest, innovation-fuelled growth bonanza. Such strong demand elevated this TA to fourth place, with a deal value share of 9%, while it was only second to oncology by deal volume, with a share of 22% (see Table 1).

Table 1: Cardiometabolic-focussed M&A deals in 2023

| Acquirer | Target | Indication | Total deal value (M) |

| Roche | Carmot Therapeutics | Obesity, T1D, T2D | $3,100 |

| Sanofi | Provention Bio | T1D | $2,815 |

| Lilly | Versanis | Obesity, heart failure | $1,925 |

| AstraZeneca | CinCor | Hypertension, CKD | $1,635 |

| Chiesi | Amryt | Lipid disorders, HoFH | $1,429 |

| Novo Nordisk | Inversago | Obesity, metabolic disorders | $1,075 |

Overall, 2023 turned out as a very reasonable year for biopharma M&A, however, we did not see deal activity roaring back to the frantic levels of 2019.

As 2024 gets underway, the fundamentals in support of dealmaking continue to be strong:

In addition to these strong fundamentals, there are incremental positive catalysts to provide further support for deal momentum in 2024:

Despite such a positive sentiment, some uncertainties remain which may result in potential headwinds for M&A momentum in 2024.

A more benign interest rate outlook for 2024, especially as signalled by the U.S. Federal Reserve, will improve the funding environment for EBPs. However, its overall impact on biopharma M&A is more nuanced, as opposing forces play out:

As in 2023, the Federal Trade Commission’s (FTC) more activist stance continues to be a source of uncertainty for dealmakers in 2024. Once focused on direct competition, especially scrutinising the impact of large transactions, the FTC now applies a wider lens to how it assesses the impact of deals on pharma companies’ negotiating power.

Ultimately, we expect greater FTC scrutiny will impact specific deals, or deal types, rather than discouraging M&A activity across the board, while dealmakers will proactively navigate potential regulatory risks.

The broader geopolitical outlook for 2024 remains challenging, e.g., ongoing conflicts, the U.S.-China strategic rivalry or the wider deglobalisation creating new barriers to cross-border sourcing of bio-medical innovation and its commercialisation. The outcome of the U.S. presidential election in November 2024, and its impact on the direction of both foreign and domestic policies, represents another, major unknown for public markets. Collectively, these incremental uncertainties will weigh on dealmaking sentiment.

Considering the dynamic interplay of all these factors that we elaborated on, including strong fundamentals, incremental catalysts, remaining uncertainties and potential headwinds, on balance our outlook for 2024 is more bullish compared to 2023.

Therefore, at this point in time, we forecast aggregate M&A deal value to reach $180-200Bn in 2024.

As for deal focus in 2024, we expect a preference for bolt-on acquisitions and de-risked assets to continue, while cardio-metabolism/obesity is likely to cement its new-found popularity alongside acquirers’ perennial favourites oncology and immunology.

Finally, while we have focused on M&A transactions in this blog, it is important to note that other deal types – beyond taking outright ownership of target companies or assets – will also play a vital role, such as licensing agreements, joint ventures, collaborations and (R&D) partnerships, as dealmakers navigate the entire risk spectrum in pursuit of future growth.

Acknowledgements

The authors would like to thank Aaron Wright and Helena Bayley for their analytical support to developing this blog.

Key data and information sources

IQVIA Pharma Deals; IQVIA Forecast Link; IQVIA Pipeline Link; Mergermarket; Refinitiv Workspace; company financial reports; company press releases and deal announcements; IQVIA EMEA Thought Leadership desk research and analysis

Maximize your healthcare investments, with evidence.

See how we partner with organizations across the healthcare ecosystem, from emerging biotechnology and large pharmaceutical, to medical technology, consumer health, and more, to drive human health forward.