Cardiovascular Clinical Research

Discover new approaches to cardiovascular clinical trials to bring game-changing therapies to patients faster.

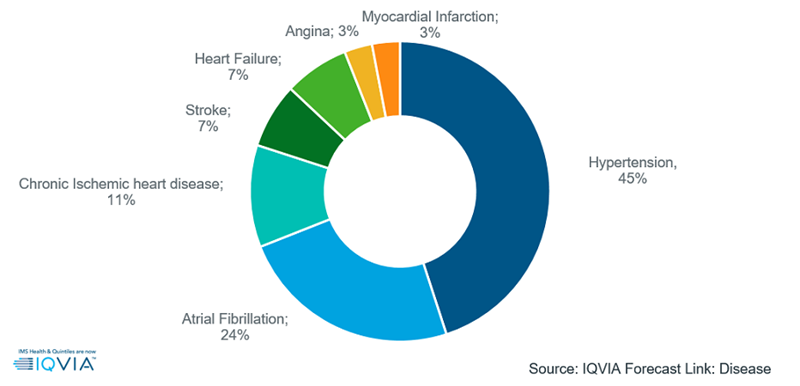

Cardiovascular Diseases (CVD) are a group of disorders affecting the heart and blood vessels and are the most common cause of death globally. According to WHO1, CVD contributed to approximately 31% or 17.9 million death globally in the year 2016. According to IQVIA’s Forecast Link, some of the major diseases that contribute to CVD based on sales are:

Although the causes of the many different types of CVD are not clear-cut, the risk of getting these heart diseases increases when an individual is suffering from high blood pressure, high cholesterol, or diabetes or is obese or has a family history of CVD. Risk also increases with age and lifestyle behaviors such as smoking, alcohol abuse or inactivity.

There is a wide range of medications available for heart disease, a number of which are taken for chronic use. Examples include:

According to Forecast Link, the market for major heart disease prescription drug sales contributed $67 billion in 2018 and has only grown at a CAGR of 0.6% since 2014, mainly due to the significant generic erosion of a blockbuster hypertension brand from late 2013. However, going forward, this market is expected to grow at a CAGR of 5.5% (2018-24) post which impending loss of protection (LoP) and generic entry will decrease the market growth at a CAGR of -2.2% (2024-28).

The hypertension market is the biggest among the other heart diseases with prescription drug sales contributing $32 billion in 2018, and is expected to grow at a CAGR of 1.7% to 2028. This is followed by atrial fibrillation which had the second-highest sales of $18 billion in 2018 and will maintain its position out to 2028, growing at a CAGR of 1%. The heart disease market forecast for 2028 is shown in Figure 1.

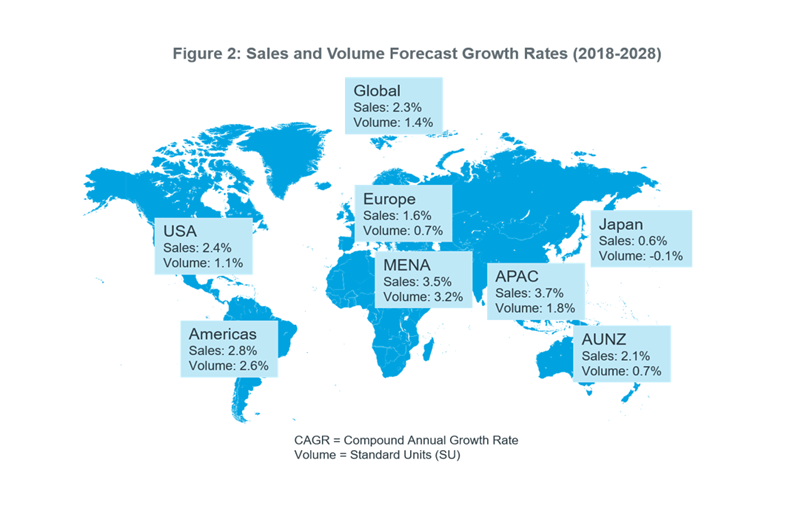

The US is the biggest market for heart disease and will continue to dominate in 2028 totalling $26.7 billion sales owing to their higher cost of treatments. In terms of percentage contribution in sales it accounts for 32% in 2028 and is expected to grow at a CAGR of 2.4% from 2018 to 2028.

Europe and APAC will also see healthy growth in terms of heart disease market while the market in Japan, MENA and AUNZ will be stable. Europe and APAC are expected to account for 27% and 22% of the global market respectively, and the remaining regions will contribute 20% in 2028.

In terms of sales growth percentages, maximum growth in sales will be seen in APAC countries, driven by new launches and an increase in number of patient days. While on the volume front, MENA will observe the highest growth followed by Americas. Drug treated patient-days volume is forecast to show slight growth, with an average global growth of 1.4% over the next 10 years. Sales and volume forecast growth rates from 2018 to 2028 is shown in Figure 2.

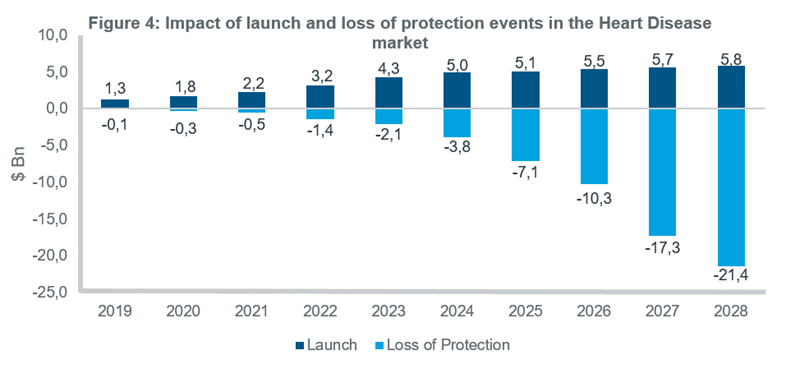

According to Forecast Link, the heart disease market will see as many as 25 launch events take place by 2023. The impact of these new launches will expand the market by approximately $5.8 billion in 2028 (Figure 3). However, due to the impending LoP of some key drugs and the consequent entry of low-priced generics, there will be a net reduction in the global market of over $21.4 billion in sales, by 2028. IQVIA’s Forecast Link predicts that at least 137 LoP events will take place between 2019-2028.

As of 2018, 32% of the drugs in being taken by patients for CVD were generics while branded products contributed to 64%. However, there will be a shift in this trend over the next 10 years as the proportion of generic use increases, with as much as 44% being generic by 2028. Even with the launch of 25 new molecules in this disease area, the loss of protection of 137 brands will see the usage of generics among patients greatly increase. Unless new therapies are introduced into the market, the dominance of generics will pertain, and some geographies may observe declining sales in this disease area.

https://www.who.int/cardiovascular_diseases/world-heart-day/en/

https://www.heart.org/en/health-topics/heart-attack/treatment-of-a-heart-attack/cardiac-medications

IQVIA Forecast Link: Disease will provide you with up-to-date forecasts for your disease of interest, so that you can measure new market opportunities and power your strategic decision making. To find out more, please visit Forecast Link: Disease.

Discover new approaches to cardiovascular clinical trials to bring game-changing therapies to patients faster.

Specialized expertise and customized solutions across 14 therapeutic centers of excellence, including oncology, GI/NASH, pediatrics, neurology and rare diseases.