Concept and Strategy Development

Illuminate a path to consumer health success

In 2020, COVID created chaos across the global consumer health market. Emerging and developed markets saw revenues fall. While we experienced some rebound in 2021, Delta and Omicron slowed that recovery. We are confident, however, that in 2022 the rebound will be stronger and more sustained. While there will be unevenness across markets, trends are indicating a good overall performance in line with 2018.

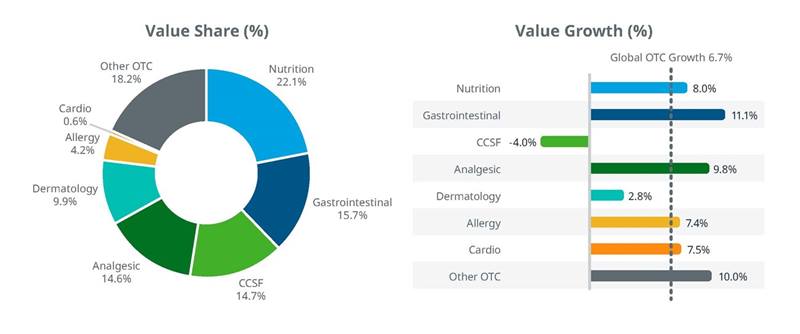

The global Over the Counter (OTC) consumer health market is going through a big recovery. After a rough 2020 due to the pandemic, 2021 saw 6.7% growth, led by nutrition and gastrointestinal categories, according to IQVIA Consumer Health’s Global OTC Insights data (see Exhibit 1). Analgesics also picked up significantly. The cough cold category, which was hardest hit during the pandemic, was still behind at -4%, but we expect that to flatten in 2022. Consumers are also investing more in health and wellness products, which creates opportunities for manufacturers to increase sales and to address evolving consumer demands.

Exhibit 1: Global OTC Category Performance – YTD November 2021, including estimates for e-Commerce and mass-market (Source: Global OTC Insights – IQVIA Consumer Health)

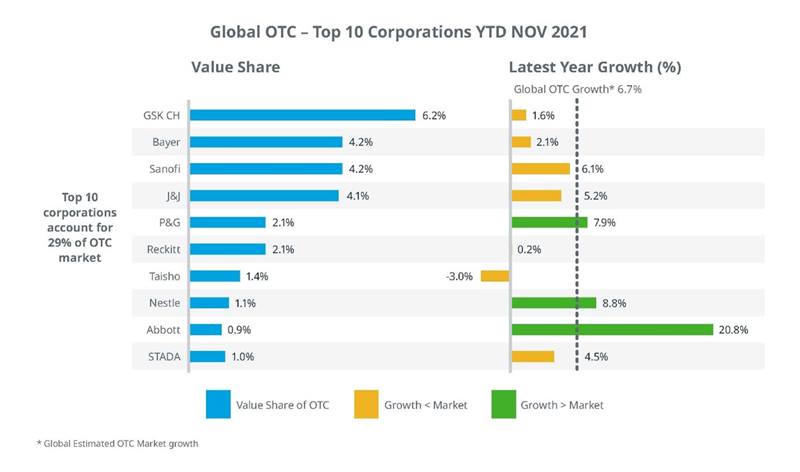

Manufacturer performance was mixed, with only P&G - driven by Digestive Health (Pepto-Bismol, Metamucil, Align probiotics), VMS (Bion, Neurobion) and by Zzzquil – in the Top 5 growing ahead of the market. Abbot was the stand-out performer across the Top 10 – which account for 29% of the market - thanks to a very strong showing from its Pedialyte, Duphalac and Creon digestive brands.

Exhibit 2: Performance of Top 10 Consumer Health Corporations YTD November 2021, including estimates for e-Commerce and mass-market (Source: Global OTC Insights – IQVIA Consumer Health)

Over the next five years, we see this recovery continuing, with varying rates of growth across markets and product categories, based on a number of trends:

Post-Covid economics

From a global standpoint, market recoveries will continue to be tied to inflation rates and Covid-19.

The Northern hemisphere has seen mass vaccination and booster rates which is allowing economies to return to a relative state of normal. But vaccination rates are still lower than desired in South America, Africa, and some parts of Middle East. That will continue to be a drag on the consumer health industry because re-openings and elimination of mask mandates will be slower in these parts of the world.

The response to Covid-19 caused healthcare spending as a percentage of GDP to soar, which could be a good thing for the OTC market. Governments will need to recover that deficit, either through taxation or cutting expenditure in other areas.

This need to cut healthcare budgets and insurance costs could see a push to shift the cost of medicines for certain long-term, but self-treatable, chronic conditions to the user by removing them from reimbursable status or by making certain medications – statins for example – available without a prescription.

As a result, new opportunities to expand the consumer health products market could arise, through new categories or by expanding existing areas.

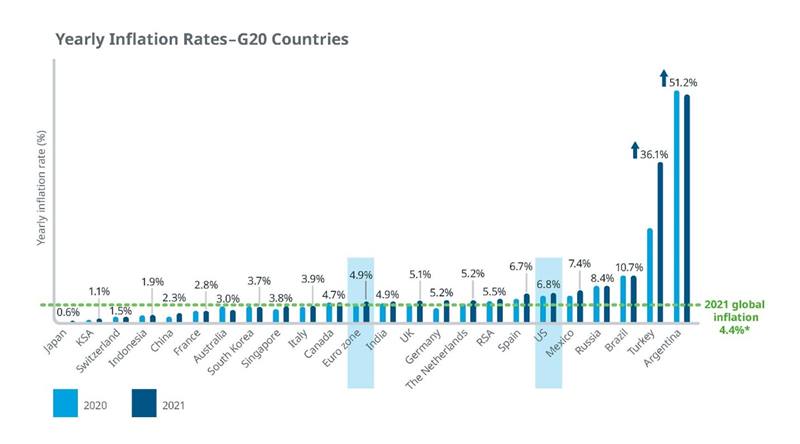

However, these opportunities could be hampered by rising costs. Raw material prices continue to increase due to inflation, which will likely require price hikes for consumer health products. Manufacturers will have to determine how to achieve a balance between costs, revenues, and competition in the marketplace (see Exhibit 3).

Exhibit 3: Yearly inflation rates across the G20 countries in 2020 and 2021 (Source: Sources: www.tradingeconomics.com; www.statista.com)

Blurred lines

As companies look for ways to gain a competitive advantage in the new Consumer Health marketplace, we are seeing an acceleration in the move to digital channels for both marketing and selling healthcare products.

We continue to see a blurring of lines between in-store and ecommerce shopping. This trend began before the pandemic, but COVID accelerated consumers’ willingness to engage with digital services and sales using mobile technology. IQVIA Consumer Health’s e-Pharmacy data shows that already around a fifth of consumer health sales in the US, Germany, and China now goes through e-Pharmacies and other e-Commerce channels.

This doesn’t mean brick-and-mortar shops will disappear. But it will require a more cohesive sales and marketing strategy, where e-Pharmacies, independent pharmacies, chains, and wholesalers work collaboratively to offer a seamless omnichannel brand experience.

AI, analytics and apps

The rise of digital sales and marketing will have long-lasting implications for the consumer health marketplace. Smaller firms are discovering new leverage via digital sales as scale is no longer a leading advantage. They can more easily pivot to meet consumer needs, which may give them a competitive edge in the future. Large companies can respond by using their access to market data and advanced analytics to stay ahead of these nimble competitors.

The use of analytics tools that leverage artificial intelligence and machine learning (AI/ML) can help companies predict future trends, optimize costs, and adapt their market strategies to changing consumer behavior. There is also an opportunity for personalization in these digital engagements, as consumers generate more data about their individual needs and health status.

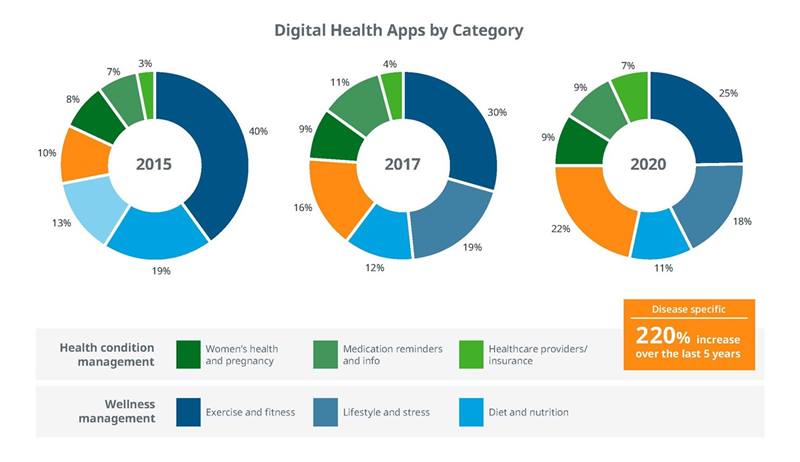

In 2020, disease-specific apps represented 22% of all apps in the marketplace (see Exhibit 4). Of those, the leading topics include mental health, digestive, respiratory, musculoskeletal pain, eyes, and ears, which align with consumer health product categories. This confluence of data and product categories offers new opportunities for manufacturers to integrate analytics more fully into their annual planning and implementation strategies.

Exhibit 4: Breakdown of digital health apps by type (Source: Source: 42 Matters, Jun 2021 and Jul 2017; Mevvy, Jun 2015; IQVIA AppScript App Database, Jun 2021; IQVIA Institute, Jun 2021)

These apps generate mountains of healthcare data that consumer health companies can use to hone market strategies, adapt them for different populations, and to time their delivery to deliver maximum impact.

The next five years promise to provide a strong recovery overall for consumer health. Companies that integrate local and global trend data into their market strategies will be best positioned to stay abreast of these trends, and to engage customers across regions, channels and categories.

To learn more about how IQVIA Consumer Health can help you stay ahead of consumer health trends or to arrange a call with Amit Shukla hit the Contact Us button.

Illuminate a path to consumer health success

Shape the future of consumer health.

See how we partner with organizations across the healthcare ecosystem, from emerging biotechnology and large pharmaceutical, to medical technology, consumer health, and more, to drive human health forward.