Stay ahead with the EMEA Thought Leadership insights: your source for industry-leading expertise and analysis

Blog

Your Questions Answered: Off-patent Semaglutide in 2026

Apr 07, 2026

March ushered in the first wave of off-patent competition for semaglutide, the active ingredient in Ozempic and Wegovy, marking a global turning point in metabolic medicine. The dynamics of this first wave of off‑patent entrants will be shaped not just by the cost of development, but also by regulatory classification, private‑market affordability, and innovators’ ability to segment the market with second brands and next‑generation therapies.

The following article builds upon our first, which explored different scenarios once semaglutide loses exclusivity (LOE), to answer some commonly asked questions now that the market is beginning to shape up.

Will semaglutide be considered a biosimilar or a generic?

Semaglutide exemplifies the fragmented regulatory landscape that exists between frameworks for complex molecules and biologics. Some regulators treat it as a complex generic, especially if chemically synthesised, while others lean toward biosimilar frameworks. This has commercial implications as semaglutide’s classification affects its development cost, time-to-market and pricing expectations.

The classification of semaglutide depends on each country's specific regulatory framework for polypeptides. Current EMA regulations would treat synthetic semaglutide as a generic and recombinant as a biosimilar, whereas the FDA treats any peptide chains of under 40 peptide residues as a generic, of which semaglutide (31 amino acids) and tirzepatide (39 amino acids) qualify.

With respect to the eight markets in the first wave losing exclusivity this year, they can broadly be classified as follows:

- Generic: Canada and Saudi Arabia treat semaglutide as a chemical drug irrespective of manufacturing method, requiring only bioequivalence studies.

- Biosimilar / Similar biologic: Brazil, India and South Africa classify it as a biologic. Brazil considers synthetics as a “synthetic analogue of a biologic peptide” which requires impurity, aggregates, and immunogenicity tests. India mandates local Phase III-style clinical trials for "similar biologics".

- Mixed: China classes semaglutide as a biologic if recombinant or chemical drug if synthetic, however still requires full clinical studies for all types. Turkey harmonises closely with EMA practice and so will likely treat the synthetic version as a generic and recombinant as a biosimilar.

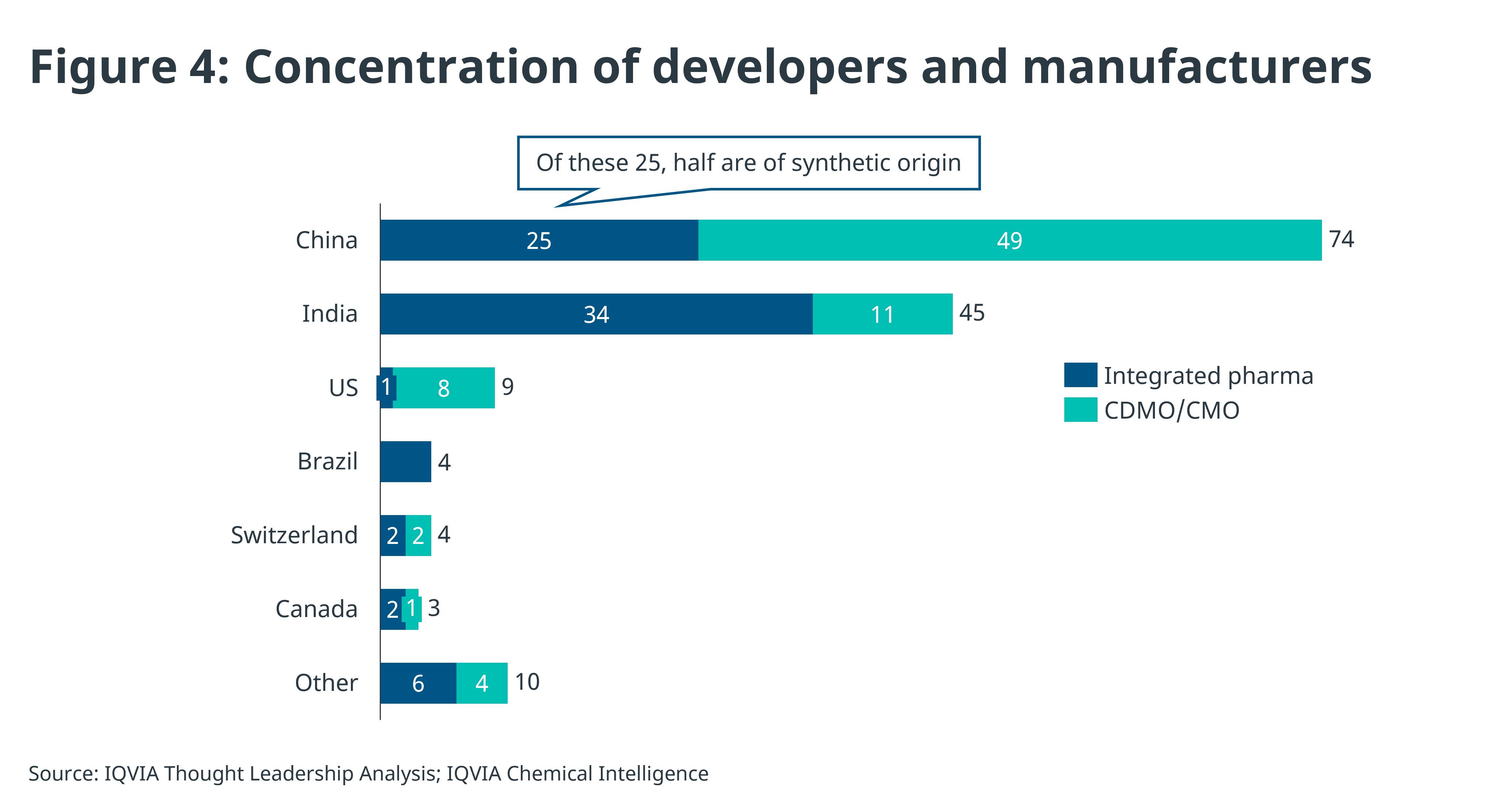

Whether a company manufactures products synthetically often depends on its current capabilities. Companies choosing synthetic production can generally access every market, while those using recombinant technology may only seek marketing approval in places where all semaglutide versions are considered biosimilars, or where exceptions allow biologics to be classified as generics. The field appears to be split across both modalities too: from the limited data made public in China, 13 of the 25 (52%) integrated pharma companies are using synthetic methods.

Which countries are losing exclusivity in 2026?

A significant wave of patent and data protection expires in 2026 across eight key markets in wave 1: Canada, Brazil, China, India, Mexico , Turkey, Saudi Arabia* and South Africa (see Figure 1).

These eight countries are particularly significant due to the diversity they offer across several critical factors: regulatory approaches, obesity prevalence, GPD per capita, population size and status as global manufacturing hubs. This provides us with a valuable analytical platform. By examining these varied environments, we can gain insights into how market dynamics might develop as subsequent waves of countries lose exclusivity, informing strategies for competitive positioning in future markets.

Going beyond 2026, the first European countries will make up the second wave of markets to lose exclusivity, starting with the Baltics and parts of Central and Eastern Europe. This second wave will be an important European proving ground for off-patent manufacturers before the third and largest wave of markets opens up, namely the US and most of Europe.

*N.B. the local patent for Saudi Arabia was never filed, so there hasn’t been a typical period of market protection. As we expect off-patent competition this year, we include it in the first wave. This may be the case for many other countries across South America, Africa and Asia which have not been included in the scope of this analysis.

What is the potential of each market?

For the majority of the following analyses, we will focus on the larger weight-loss indication to explore the potential of off-patent semaglutide in the eight countries. In aggregate, they represent a massive share of the global metabolic disease burden, accounting for 38% of the world’s adult population living with obesity (Figure 2). This creates an environment of significant demand for affordable and efficacious obesity medicines, one that has largely been served so far by the private, or out-of-pocket, market.

Across all eight markets, obesity prevalence is expected to rise through to 2050, particularly in Mexico (+18%), Brazil (+17%) and Saudi Arabia (+16%) demonstrating the increasing unmet need to tackle population weight.

The commercial potential will initially be driven by expansion in the private market, at least while public reimbursement remains constrained. Figure 3 shows at a high level how each country can be mapped against indicators of their ability for public reimbursement (GDP per capita) and private spend (out-of-pocket [OOP] expenditure per capita) with the size of the bubble proportional to total 2025 list-price semaglutide sales. This figure is a useful representation of demand, but real market dynamics are driven additionally by price, cultural attitudes towards aesthetic use, the regulation of online channels and home delivery, as well as many other factors that determine actual market uptake and size.

Canada is the standout country, notably a high GDP-per capita and a high exposure to OOP spend, as well as a substantial prevalence of adults living with obesity. Its reimbursement for diabetes and OOP payments for medicines are some of the driving factors to its large market size compared to the other markets in this first wave.

Saudi Arabia and Turkey are countries with a relatively high GDP per capita, as well as a high adult obesity prevalence. These countries have a comparatively lower OOP exposure: Turkey has restrictions on the online purchasing of semaglutide, reducing accessibility, and Saudi Arabia has online channels but a focus on state-provisioned healthcare over OOP payments signals their cultural, and structural propensity to rely less on the private market.

The cluster of India, China and Mexico show high differences in prevalence but contain a high level of absolute number of potential patients indicating their important size, coupled with high OOP exposure. These markets are expected to be volume drivers, particularly in the private market.

The final cluster of India and South Africa represent price-sensitive volume drivers. Particularly India, although a lower adult obesity prevalence, has a large absolute number of patients and prices have already fallen by up to 90% (see pricing section below) in what looks to be a highly competitive market.

The potential for public reimbursement is a combination of unmet need, driven by obesity prevalence, which drives focus on the disease, and the nation’s ability to fund treatments. High prevalence is a double-edged sword, as it raises awareness and a mandate to tackle the disease, but the high proportion of the population receiving public care could be cost-prohibitive, leading health systems to restrict eligible patients by focusing on severity or comorbidities as they are currently doing with the protected innovative brands.

Who are the major players?

There is increasing clarity on the competitors preparing to enter these markets, though entry will be staggered due to delays from regulatory complexity, volume of submissions, and manufacturing hiccups. IQVIA has identified over 70 integrated pharma companies applying for marketing authorisation and an additional 70 companies that are able to manufacture the semaglutide API for third parties, see Figure 4.

Contract manufacturers (CDMO/CMOs) are typically API manufacturers, some with fill & finish capabilities that will be looking to provide manufacturing services, but not seek to enter markets themselves, whereas integrated developers have existing manufacturing capabilities and will apply for marketing authorisation in their countries of interest.

China has the highest concentration of semaglutide manufacturing across both integrated developers and CDMOs, clearly ahead of other countries in peptide manufacturing, whereas India is in second place, but importantly contains the greatest number of integrated pharma companies with existing international reach such as Biocon, Dr. Reddy’s and Lupin. This international reach matters as they will have a track record in GMP, dossier preparation and a network in first wave markets.

Most companies are simultaneously developing oral and vial versions of semaglutide to circumvent the need for the use of pens. These come with their own complications around formulation for bioequivalence, stability, and loss of exclusivity which brings ambiguity to market access for those companies not able to secure a supply of pens.

What will happen to prices?

The question of pricing of off-patent semaglutide is one with many opinions and little hard fact at present. A recent study by Professor Andrew Hill et ali suggests that finished forms of semaglutide pens can be sold to patients for anything between $2.50-$12 per month, but this underestimates a large number of costs associated with sourcing from diverse geographies, as well as costs during the market access process.

Moreover, Professor Hill’s study assumes a cost-plus model which is not the standard pricing framework employed by most companies. Hill's study sets a (possibly theoretical) floor price but other considerations, including competition, willingness to pay and the need for commercial return on capital expenditure will shape pricing realities.

Hill’s research does suggest that, while the API is a minor cost component compared to the pen in an injectable formulation, the need to dose daily for a higher API load in a pill makes orals pricier to manufacture than injectables, further raising the competitive advantage of manufacturing small molecule alternatives, such as Lilly’s orforglipron.

In general, prices are expected to fall due to increased competition, but how far and how fast will differ by market and by channel separation (public vs private pricing divergence).

In India, prices have already fallen significantly, with multi-dose vials priced as low as $14 per monthii and disposable pens at $19 per monthiii for the lowest dose forms, a discount of up to 90%.

Figure 5 consolidates country submissions, formal pricing rules, and expected entrants to gain a qualitative assessment of expected pricing pressure. This is mapped against the current private prices for the highest maintenance dose of semaglutide for obesity (2.4mg injection) as a benchmark.

Canada is currently the market among the first wave with the highest rates of public reimbursement for semaglutide, though it is limited to type 2 diabetes (T2D). In this segment, once three generics of an injectable are on the market, the price must legally fall to 35% of the brand price (a 65% cut). Moreover, aside from Novo Nordisk’s own second brands, around 5 applicants have filed for generic entry, including Apotex, Sandoz, and Teva – well capitalised players that are able to navigate the sophisticated market access environment.

As China and India host nearly 80% of developing companies, we can expect the competitive pressure to be high in these traditionally price-sensitive markets. China also lists semaglutide in its national reimbursement list (NRDL) for T2D which will increase top-down pressure for switching to the off-patent version.

Brazil’s regulator, ANVISA, recently announcediv it has 17 products currently under review, of which 15 are synthetic and 2 are of recombinant origin.

Saudi Arabia and Mexico, even though they have a high obesity prevalence, will likely experience less pricing pressure than other markets. Mexico, due to a lesser number of competitors aiming to enter the market immediately, and competitive damping due to Saudi Arabia’s regulatory complexity and favouring of local manufacturing giving greater weight to those companies with local operations. Novo Nordisk has partnered with Lifera (April 2025), a Saudi-funded biotech platform, to localise manufacturing as part of Saudi’s National Biotech Strategy and is expected to be a preferred supplier.

Despite the high number of competitors across the board, delays are expected and launches will be staggered, providing a phased competitive environment. Regulatory requirements for Phase III trials in China and Turkey, evaluating a complex molecule as a generic in Canada, or manufacturing issues, such as water quality consistency in Saudi Arabia, has already contributed to these delays.

How will innovators respond?

Innovator companies will use three main levers to defend and expand their share post-semaglutide LOE:

- Near-term: Second brands/authorised alternatives. Novo Nordisk has launched or is planning on launching secondary brands in 4 of the 8 markets in the first wave. In doing so, it aims to reach price-sensitive segments or compete directly with generics. Lilly’s tirzepatide has gained a strong reputation for efficacy in these markets, and while evidence is limited, in Indiav it has signalled that it will attempt to maintain premium pricing rather than compete against the off-patent offerings.

- Near/Mid-term : Oral formulations. Oral formulations not only have advantages of convenience over injectables but also bypasses the need for the cold chain , and the need to secure a large supply of injectable pens – which the majority of off-patent companies do not manufacture in-house. Novo Nordisk has highlighted strong early uptake for its obesity pill in the US in early 2026 , framing oral semaglutide in obesity as part of its growth strategy beyond injectables. Lilly will be launching small molecule orforglipron in late 2026 following an FDA PDUFA date in April, having built over $1bn in inventory as it anticipates high demand.

- Long-term: Next-generation drugs. In the near term, Novo Nordisk expects FDA approval for its semaglutide successor CagriSema (cagrilintide + semaglutide), a GLP-1/amylin combination, in late 2026. CagriSema recently demonstrated lower weight-loss against tirzepatide (REDEFINE-1 trial), but by all intents and purposes will be competitive at the right price-point. Boehringer Ingelheim is expected to be the third player in this space with their launch of survodutide in the first half of 2027. Further into 2027 and beyond, both Novo Nordisk and Lilly will be launching a suite of newer generation medicines, including Lilly’s highly anticipated retatrutide. Additional players entering the market with their own innovative offerings include Roche, Pfizer, AstraZeneca and Amgen.

What are the strategic implications for players in 2026/27?

- Earlier waves informing later ones. The first wave of markets losing exclusivity will inform decisions for waves 2 and 3, the larger US and European markets, where the stakes are highest. These decisions will centre on positioning new entrants, whether off-patent semaglutide or next-generation obesity medicines, in an increasingly crowded field. Metrics players should observe include time-to-approval, private price erosion, reimbursement triggers, and affordable vs premium segmentation.

- Canada as a template for developed countries. European countries and the US will observe how Health Canada deals with a large volume of applications for a ‘complex generic’ as well as pharmacy substitution dynamics to increase uptake. Moreover, guidance may relax to increase public uptake. Companies will be able to analyse how private market dynamics reorganise on off-patent semaglutide entry to validate hypotheses regarding patient segmentation across the wider choice of brands.

- Price elasticity of semaglutide. Canada has the most OOP exposure as well as a moderately high obesity prevalence, on the other hand India has a lower OOP exposure but a highly competitive field. This will give us insights on the relationship between price and volume in the private market for the weight-loss indication across diverse markets.

- The volume engines. Brazil, Mexico will initially drive volume due to the relatively high obesity prevalence in these countries combined with a high absolute population. There will be gradual adoption from China and India, countries with a lower prevalence, that will then drive absolute volume due to their sheer size albeit at a lower price point due to high competition. In the public market, regulators that approve semaglutide as a biosimilar may experience slower uptake as automatic substitution rules are usually restrictive.

- Innovation vs. access. Oral GLP-1s and next generation medicines demonstrating higher clinical efficacy or tolerability will likely be positioned to capture premium segments, whereas the bulk of growth in price-sensitive markets like India, China, and Mexico will favour low-cost semaglutide.

References

i How Low Could Semaglutide Prices Fall? An Analysis of Production Cost and Implications for Global Access Ahead of Patent Expiry; https://doi.org/10.64898/2026.03.04.26347508