-

Americas

-

Asia & Oceania

-

A-I

J-Z

EMEA Thought Leadership

Developing IQVIA’s positions on key trends in the pharma and life sciences industries, with a focus on EMEA.

Learn more -

Middle East & Africa

EMEA Thought Leadership

Developing IQVIA’s positions on key trends in the pharma and life sciences industries, with a focus on EMEA.

Learn more

Regions

-

Americas

-

Asia & Oceania

-

Europe

-

Middle East & Africa

-

Americas

-

Asia & Oceania

-

Europe

Europe

- Adriatic

- Belgium

- Bulgaria

- Czech Republic

- Deutschland

- España

- France

- Greece

- Hungary

- Ireland

- Israel

- Italia

EMEA Thought Leadership

Developing IQVIA’s positions on key trends in the pharma and life sciences industries, with a focus on EMEA.

Learn more -

Middle East & Africa

EMEA Thought Leadership

Developing IQVIA’s positions on key trends in the pharma and life sciences industries, with a focus on EMEA.

Learn more

SOLUTIONS

-

Research & Development

-

Real World Evidence

-

Commercialization

-

Safety & Regulatory Compliance

-

Technologies

LIFE SCIENCE SEGMENTS

HEALTHCARE SEGMENTS

- Information Partner Services

- Financial Institutions

- Public Health and Government

- Patient Associations

- Payers

- Providers

THERAPEUTIC AREAS

- Cardiovascular

- Cell and Gene Therapy

- Central Nervous System

- GI & Hepatology

- Infectious Diseases and Vaccines

- Oncology

- Pediatrics

- Rare Diseases

- View All

Impacting People's Lives

"We strive to help improve outcomes and create a healthier, more sustainable world for people everywhere.

LEARN MORE

Harness the power to transform clinical development

Reimagine clinical development by intelligently connecting data, technology, and analytics to optimize your trials. The result? Faster decision making and reduced risk so you can deliver life-changing therapies faster.

Research & Development OverviewResearch & Development Quick Links

Real World Evidence. Real Confidence. Real Results.

Generate and disseminate evidence that answers crucial clinical, regulatory and commercial questions, enabling you to drive smarter decisions and meet your stakeholder needs with confidence.

REAL WORLD EVIDENCE OVERVIEWReal World Evidence Quick Links

See markets more clearly. Opportunities more often.

Elevate commercial models with precision and speed using AI-driven analytics and technology that illuminate hidden insights in data.

COMMERCIALIZATION OVERVIEWCommercialization Quick Links

Service driven. Tech-enabled. Integrated compliance.

Orchestrate your success across the complete compliance lifecycle with best-in-class services and solutions for safety, regulatory, quality and medical information.

COMPLIANCE OVERVIEWSafety & Regulatory Compliance Quick Links

Intelligence that transforms life sciences end-to-end.

When your destination is a healthier world, making intelligent connections between data, technology, and services is your roadmap.

TECHNOLOGIES OVERVIEWTechnology Quick Links

CLINICAL PRODUCTS

COMMERCIAL PRODUCTS

COMPLIANCE, SAFETY, REG PRODUCTS

BLOGS, WHITE PAPERS & CASE STUDIES

Explore our library of insights, thought leadership, and the latest topics & trends in healthcare.

DISCOVER INSIGHTSTHE IQVIA INSTITUTE

An in-depth exploration of the global healthcare ecosystem with timely research, insightful analysis, and scientific expertise.

SEE LATEST REPORTS

FEATURED INNOVATIONS

-

IQVIA Connected Intelligence™

-

IQVIA Healthcare-grade AI™

-

Human Data Science Cloud

-

IQVIA Innovation Hub

-

Decentralized Trials

-

Patient Experience powered by Apple

WHO WE ARE

- Our Story

- Our Impact

- Commitment to Public Health

- Code of Conduct

- Environmental Social Governance

- Privacy

- Executive Team

NEWS & RESOURCES

Unlock your potential to drive healthcare forward

By making intelligent connections between your needs, our capabilities, and the healthcare ecosystem, we can help you be more agile, accelerate results, and improve patient outcomes.

LEARN MORE

IQVIA AI is Healthcare-grade AI

Building on a rich history of developing AI for healthcare, IQVIA AI connects the right data, technology, and expertise to address the unique needs of healthcare. It's what we call Healthcare-grade AI.

LEARN MORE

Your healthcare data deserves more than just a cloud.

The IQVIA Human Data Science Cloud is our unique capability designed to enable healthcare-grade analytics, tools, and data management solutions to deliver fit-for-purpose global data at scale.

LEARN MORE

Innovations make an impact when bold ideas meet powerful partnerships

The IQVIA Innovation Hub connects start-ups with the extensive IQVIA network of assets, resources, clients, and partners. Together, we can help lead the future of healthcare with the extensive IQVIA network of assets, resources, clients, and partners.

LEARN MORE

Proven, faster DCT solutions

IQVIA Decentralized Trials deliver purpose-built clinical services and technologies that engage the right patients wherever they are. Our hybrid and fully virtual solutions have been used more than any others.

LEARN MORE

IQVIA Patient Experience Solutions powered by Apple

Empowering patients to personalize their healthcare and connecting them to caregivers has the potential to change the care delivery paradigm. IQVIA and Apple are collaborating to bring this exciting future of personalized care directly to devices patients already have and use.

LEARN MOREWORKING AT IQVIA

Our mission is to accelerate innovation for a healthier world. Together, we can solve customer challenges and improve patient lives.

LEARN MORELIFE AT IQVIA

Careers, culture and everything in between. Find out what’s going on right here, right now.

LEARN MORE

WE’RE HIRING

"Improving human health requires brave thinkers who are willing to explore new ideas and build on successes. Unleash your potential with us.

SEARCH JOBSInstitute Report

Orphan Drugs in the United States (Part two)

Dec 18, 2018

About the Report

In the thirty-five years since the passage of the Orphan Drug Act (ODA) in 1983, the structure of development incentives laid out in the legislation has successfully spurred investment and innovation in rare disease therapies. Recent legislative discussion has focused on whether the ODA development incentives are working as intended or being manipulated for commercial gain. This report is a companion analysis to an examination of the orphan drug market published by the IQVIA Institute in October 2018, “Orphan Drugs in the United States: Growth Trends in Rare Disease Treatments,” and sheds new light on this topic with information on the sequence of orphan drugs’ orphan and non-orphan indication approvals and their associated patent and market exclusivities. It also examines orphan drug pricing relative to patient numbers, how those prices change over time, and – in a first-of-its-kind comprehensive analysis – compares current disease epidemiology to the number of treated patients to demonstrate the challenges in bringing orphan drugs to patients even after they’re approved.

Report Summary

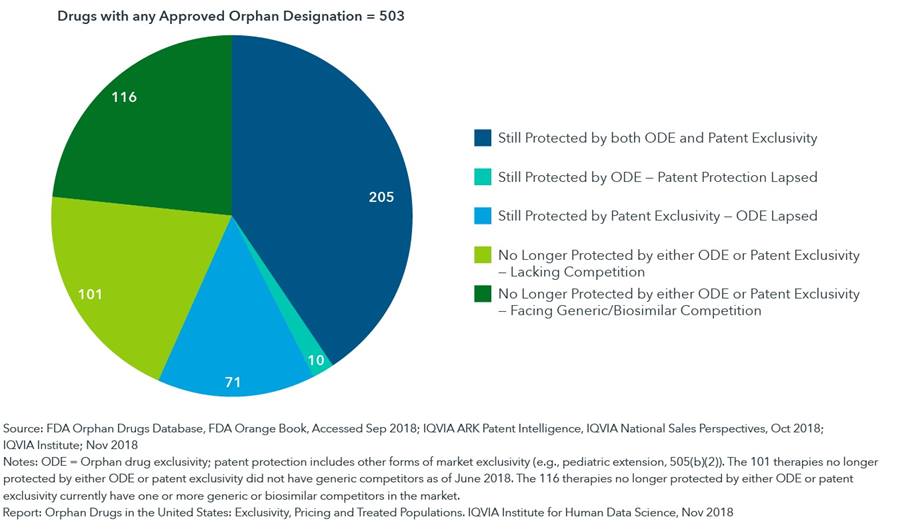

One of the key aspects of the Orphan Drug Act of 1983 is a seven-year market exclusivity granted to drugs that treat rare diseases. Since the passage of the Orphan Drug Act, a total of 503 drugs have received orphan status from the FDA. Of these, 217 drugs (43%) are now no longer protected by either orphan designations or patents, and yet only 116 (23%) of these unprotected medicines currently face generic or biosimilar competitors. This means just under half of the unprotected products still have not faced competition, some even decades after their exclusivity lapsed. The report additionally finds that it is most often the lapsing of patent exclusivity that enables competition and not the lapsing of orphan drug exclusivity.

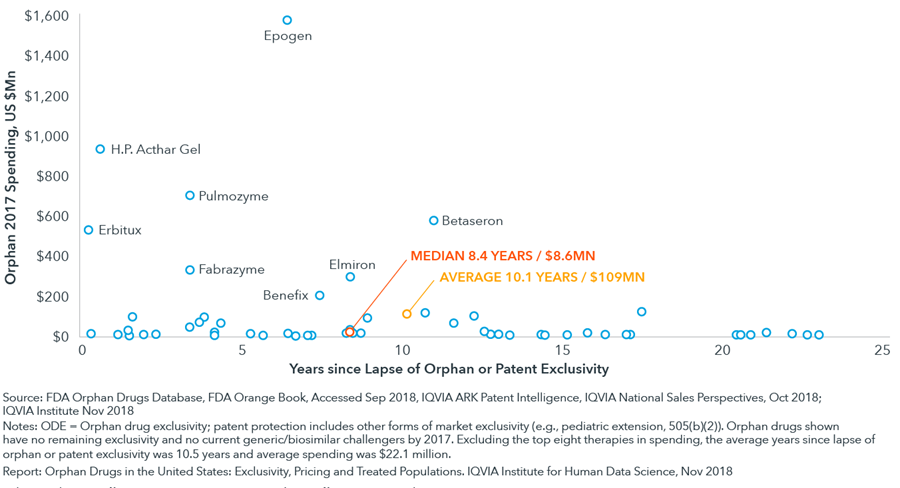

In our earlier report, “Orphan Drugs in the United States: Growth Trends in Rare Disease Treatments,” most orphan drugs were seen to have relatively low prices, and those that do have exceptionally high-prices, treat very few patients. This report builds on that analysis and demonstrates that companies have consistently raised prices for orphan drugs more slowly than other branded drugs in the market, historically, as well as in a time-aligned comparison relative to the addition of orphan status for a drug. Compared to the orphan drug market as a whole, spending on unprotected orphan drugs not experiencing generic competition is modest, with drugs on average reaching just over $100 million in spending in 2017 after approximately 10 years without a competitor. Excluding eight drugs with the greatest spending, the average spending on orphan brands not experiencing generic competition drops to just over $22 million in 2017.

A comprehensive epidemiological examination indicates that treated patients represent approximately 10% of disease prevalence for rare diseases, with notable exceptions. Generally, orphan drugs target fewer than 200,000 patients, though the actual target populations vary significantly, and around a quarter of orphan drug approvals target populations smaller than 5,000 patients in the United States. Further, some rare diseases see fewer than 1% of their prevalent patients receiving orphan medicines given that diagnosis and treatment of some rare diseases with very small populations remains complicated even in the presence of effective treatments. This demonstrates the need for a concerted effort to disseminate treatment guidance to the wider medical community and to patients once a drug is approved.

Key Findings

Of all 503 drugs that have received orphan designations, 217 are now no longer protected by either orphan exclusivity or patent designations, but only 116 of these currently face generic competitors

- With orphan designation, the FDA grants a seven-year market exclusivity which applies specifically to the designated orphan use, but this exclusivity does not preclude generic competition for other non-orphan approved uses of that drug.

- Of the orphan designated drugs, 286 remain protected by some form of exclusivity, either orphan drug exclusivity or patent exclusivity.

- Those medicines not yet facing competition are indicative of challenges that delay the number of generic challengers, such as small-revenue markets.

The median annual spending of orphan drugs no longer protected by either orphan drug exclusivity or patent protection was $8.6 million in 2017, reflecting very limited commercial opportunities for potential generic challengers

- While there is one drug in this category with more than $1 billion in spending, there are another seven with more than $200 million in spending, each of which have a unique circumstance that appears relevant to delayed or absent competition.

- Aside from the eight largest-selling drugs in this group, all had 2017 sales below $120 million and averaged just over $22 million.

- For most orphan medicines with complex or costly manufacturing or less than $20 million dollars in annual sales, it is likely that they will never face generic or biosimilar competition.

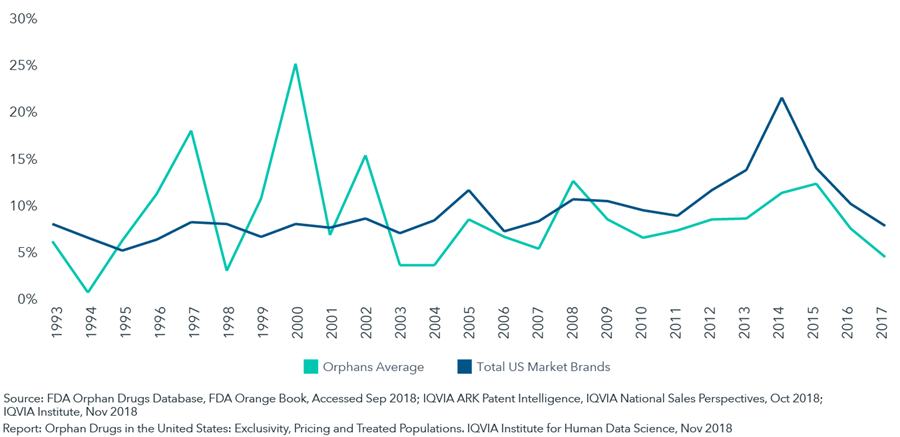

Over the past five years, orphan drugs have exhibited average price growth below the rate of the total branded market

- In looking at pricing trends over the past 25 years, price increases for orphan drugs have been lower than non-orphans for most of the last decade, while they were higher than the market in the 1990’s.

- Drugs which add an orphan designation (either at launch or after having been on the market for another use) have consistently raised prices more slowly than the market.

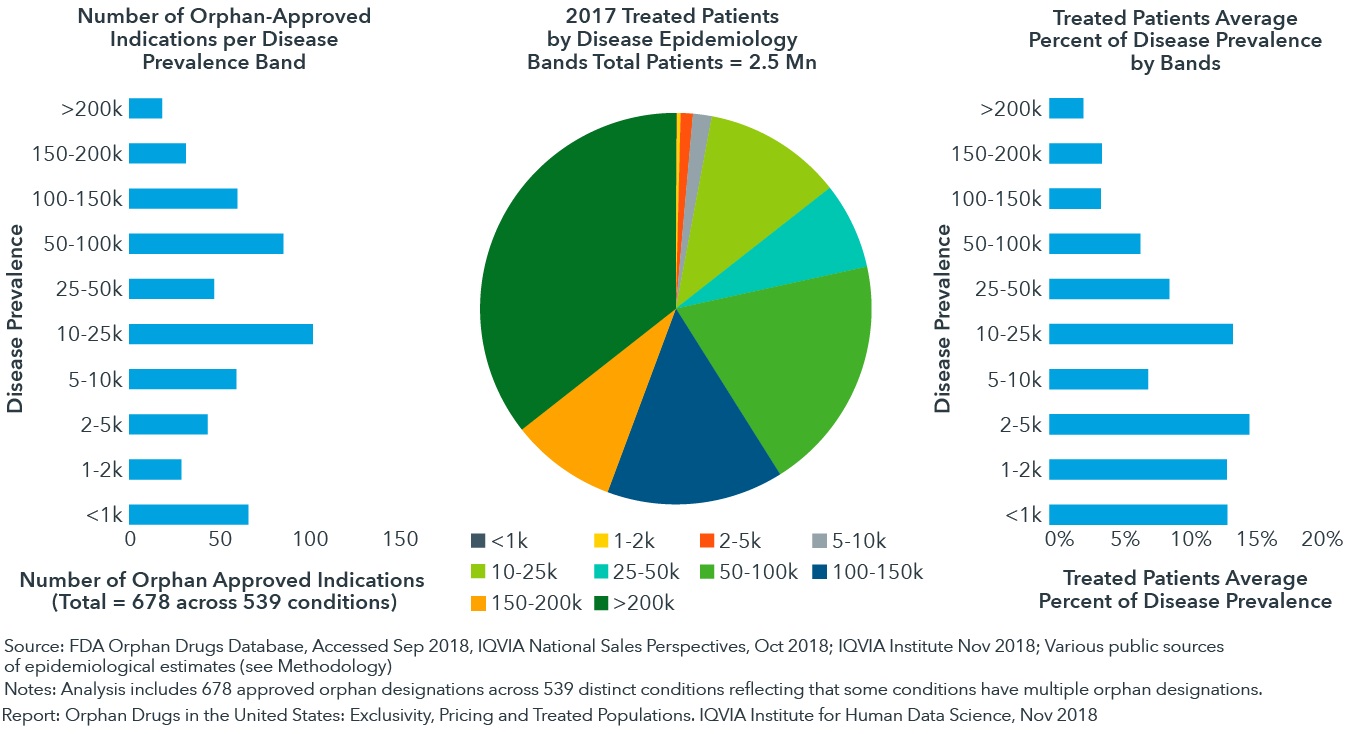

When diseases treated by orphan drugs are measured by estimated incidence or prevalence, an average of 10% of patients are receiving treatment with those drugs

- Reasons for this low drug-treatment rate include undiagnosed patients and the availability of newer non-orphan therapies that supersede older, orphan drugs.

- Approximately a quarter of approved orphan drug indications target populations smaller than 5,000.

- Treated patients for these indications with < 5,000 patients average 13.5% of disease prevalence, suggesting that identification and diagnosis of these very rare diseases is challenging.