Biosimilars

Bring your biosimilar to market faster by tapping into unparalleled data, technology, advanced analytics, and scientific expertise.

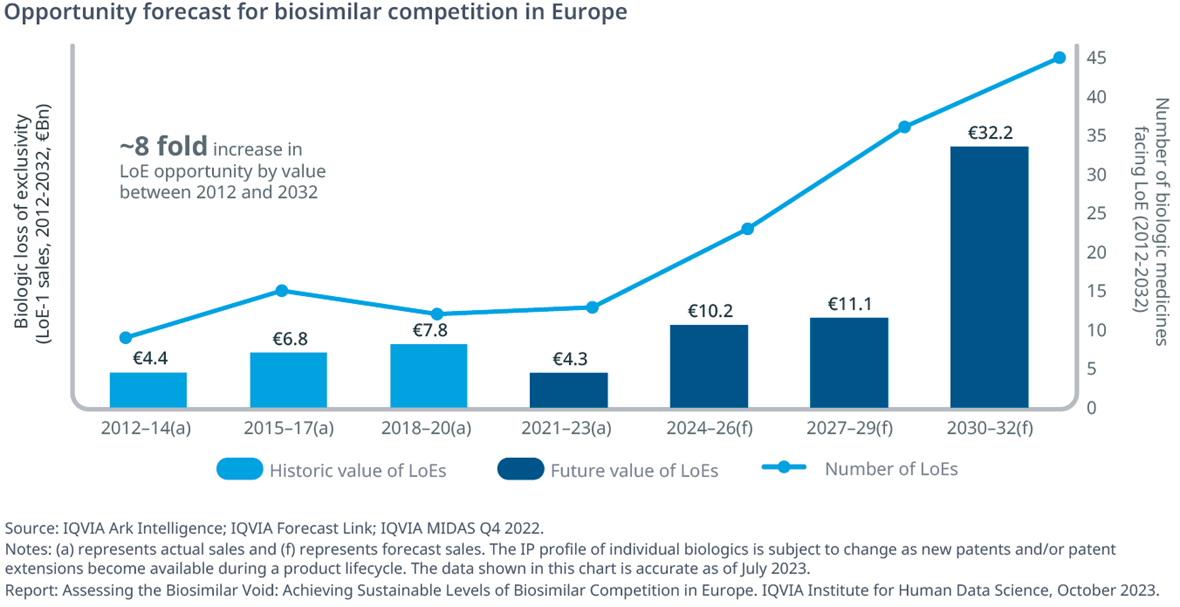

While biosimilar competition in Europe has played a vital role in achieving significant healthcare savings and expanding patient access to key medicines, the changing nature of future loss of exclusivity (LoE) events means that competition, and by extension savings, is not always guaranteed.

This report provides a timely view of the factors underlying the changing level of biologic pipeline activity in Europe, highlighting classes of biologics that are at risk of failing to attract biosimilar competition, a concept called “the biosimilar void.” This report also aims to quantify the potential impact of the biosimilar void on healthcare system budgets. Drawing on a wide range of IQVIA proprietary data and engagement with individual stakeholders, the report examines the cohort of biologic medicines that will lose protection over the next 10 years. The period for assessment (2023–2032) has been chosen to reflect the average development timeline for new biosimilar candidates (~7-10 years) and intrinsic limitations with forecasting data beyond 2032. Due to the evolving nature of the IP landscape in Europe, legal and IP barriers are not discussed in the present study.

Bring your biosimilar to market faster by tapping into unparalleled data, technology, advanced analytics, and scientific expertise.

Specialized expertise and customized solutions across 14 therapeutic centers of excellence, including oncology, GI/NASH, pediatrics, neurology and rare diseases.